Kerrigan Advisors’ 2026 OEM Survey was designed to gauge OEM executives’ perspectives on the franchise system, dealership financial performance, the dealership buy/sell market and the impact of tariffs, AI and EV adoption on US automotive retail. This one-of-a-kind survey provides a critical window into the perspectives of OEM executives whose views are not often shared publicly in the industry.

Kerrigan Advisors’ 2026 OEM Survey was designed to gauge OEM executives’ perspectives on the franchise system, dealership financial performance, the dealership buy/sell market and the impact of tariffs, AI and EV adoption on US automotive retail. This one-of-a-kind survey provides a critical window into the perspectives of OEM executives whose views are not often shared publicly in the industry.

The results of the 2026 Kerrigan OEM Survey reflect a fundamentally resilient outlook for US automotive retail among OEM executives. With tariffs forming an important backdrop to this year’s survey, executives tempered their expectations for new vehicle sales even as they continued to expect dealership blue sky values and profitability to hold firm. The survey also makes clear that OEMs anticipate a highly active buy/sell market, intend to further consolidate and more tightly manage their dealer networks, and increasingly view AI as a meaningful driver of future dealership profitability.

Dealership Valuations, Buy/Sell Activity & Profitability Outlook

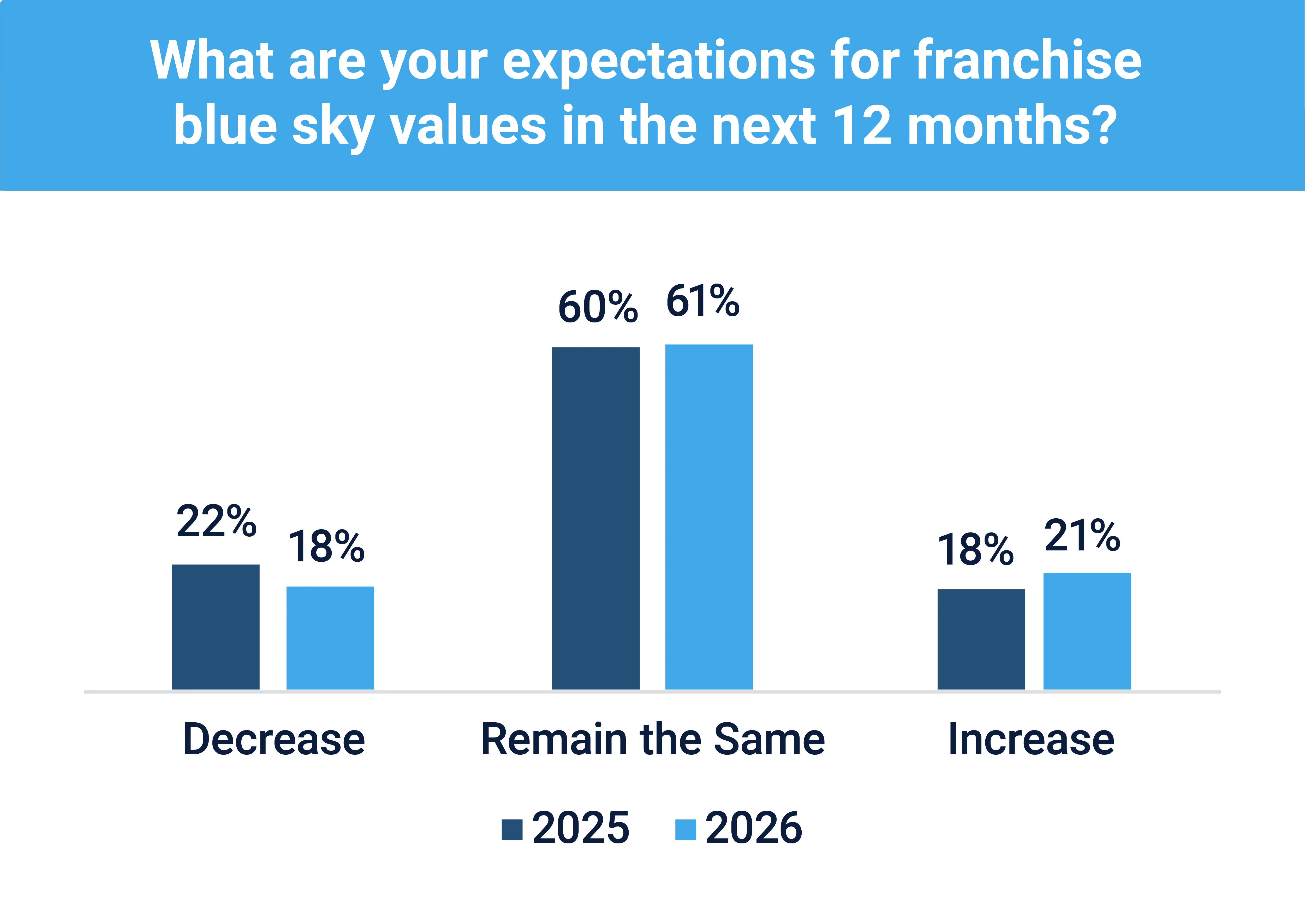

The results of Kerrigan Advisors’ fourth annual OEM executive survey indicate a more positive outlook for dealership valuations in 2026, with the vast majority of respondents expecting blue sky values to hold firm or improve in the year ahead. 61% of respondents expect blue sky values to remain the same and 21% expect an increase, while just 18% anticipate a decrease — a four percentage point improvement from the 22% who expected a decline in 2025.

For the first time, Kerrigan Advisors asked OEM executives about their expectations for buy/sell activity over the next 12 months. The results point to a robust and likely growing dealership M&A market in 2026: 35% of respondents expect more buy/sells for their franchises, 53% expect activity to continue at today’s elevated level, and only 12% project fewer transactions. Taken together, 88% of OEM executives expect buy/sell activity to hold steady or accelerate — a strong endorsement of the continued strength of the dealership buy/sell market and consistent with the record transaction activity reported in Kerrigan Advisors’ Blue Sky Report®.

Alongside their positive outlook for dealership valuations and an active buy/sell market, OEM executives are also projecting strong dealership profitability gains as AI adoption accelerates. A majority (59%) believe AI will increase dealership profits, while 37% expect no change and only 4% anticipate a decrease. This result is particularly meaningful in light of the 2025 Kerrigan Dealer Survey, which revealed that 90% of surveyed dealers are already using AI in their dealerships or plan to do so — indicating that the operational adoption required to realize these profit gains is already well underway in 2026. Kerrigan Advisors expects the wide-scale deployment of AI across dealership operations to reduce dealership selling expenses and enhance revenue per employee, thereby increasing dealers’ productivity and profitability levels.

Light Vehicle Sales Market Trends

Kerrigan Advisors also queried OEM executives about their expectations for overall market trends.

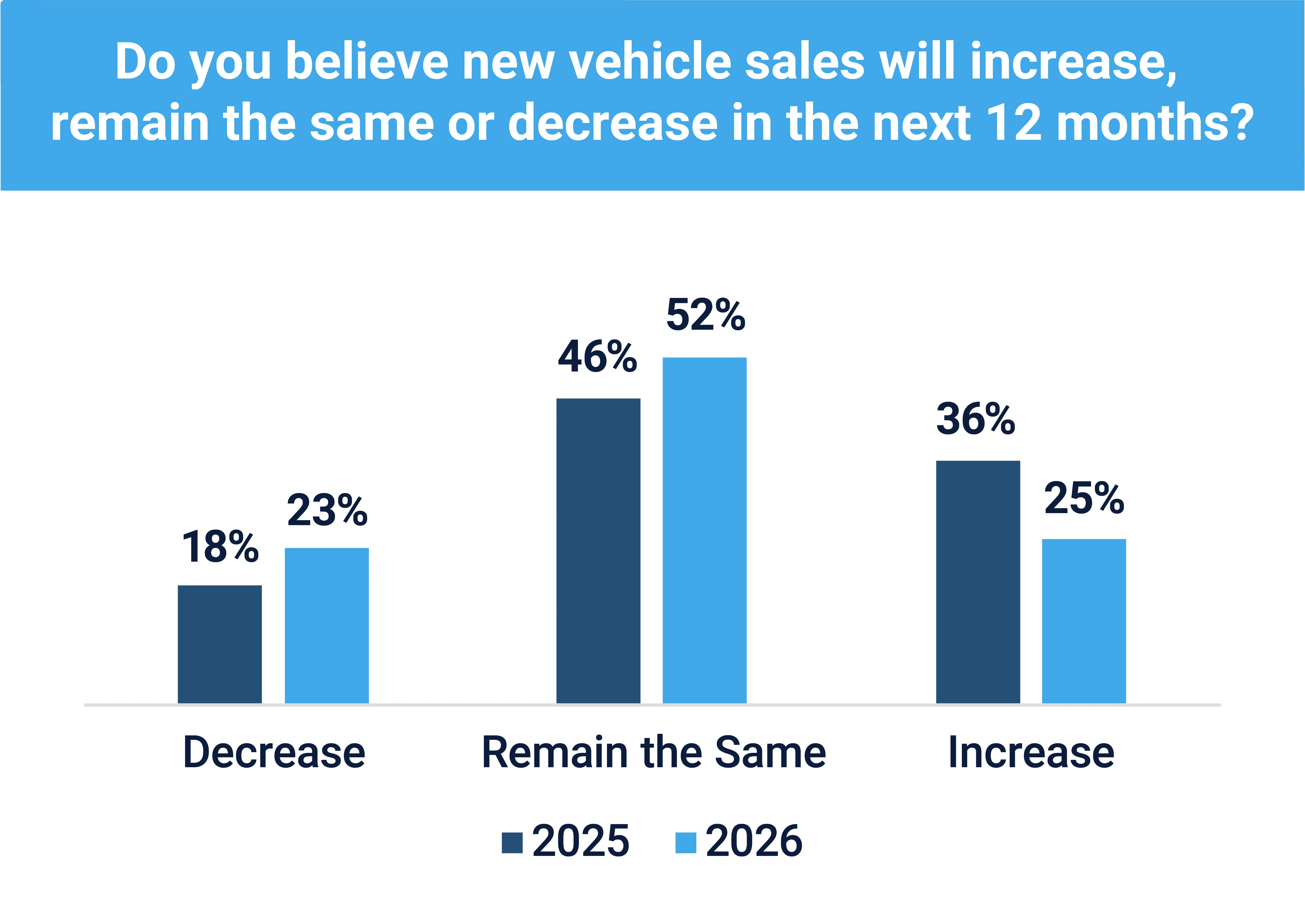

Of note, sentiment toward new vehicle sales softened meaningfully this year. While a clear majority (77%) of respondents still project new vehicle sales to remain flat or rise over the next 12 months, the share of executives anticipating a decline rose to 23%, up from 18% in 2025, while the share expecting an increase fell to 25% from 36%. Kerrigan Advisors attributes this deterioration in sales expectations to the uncertainty surrounding tariffs, weakness in EV demand and consumer affordability challenges.

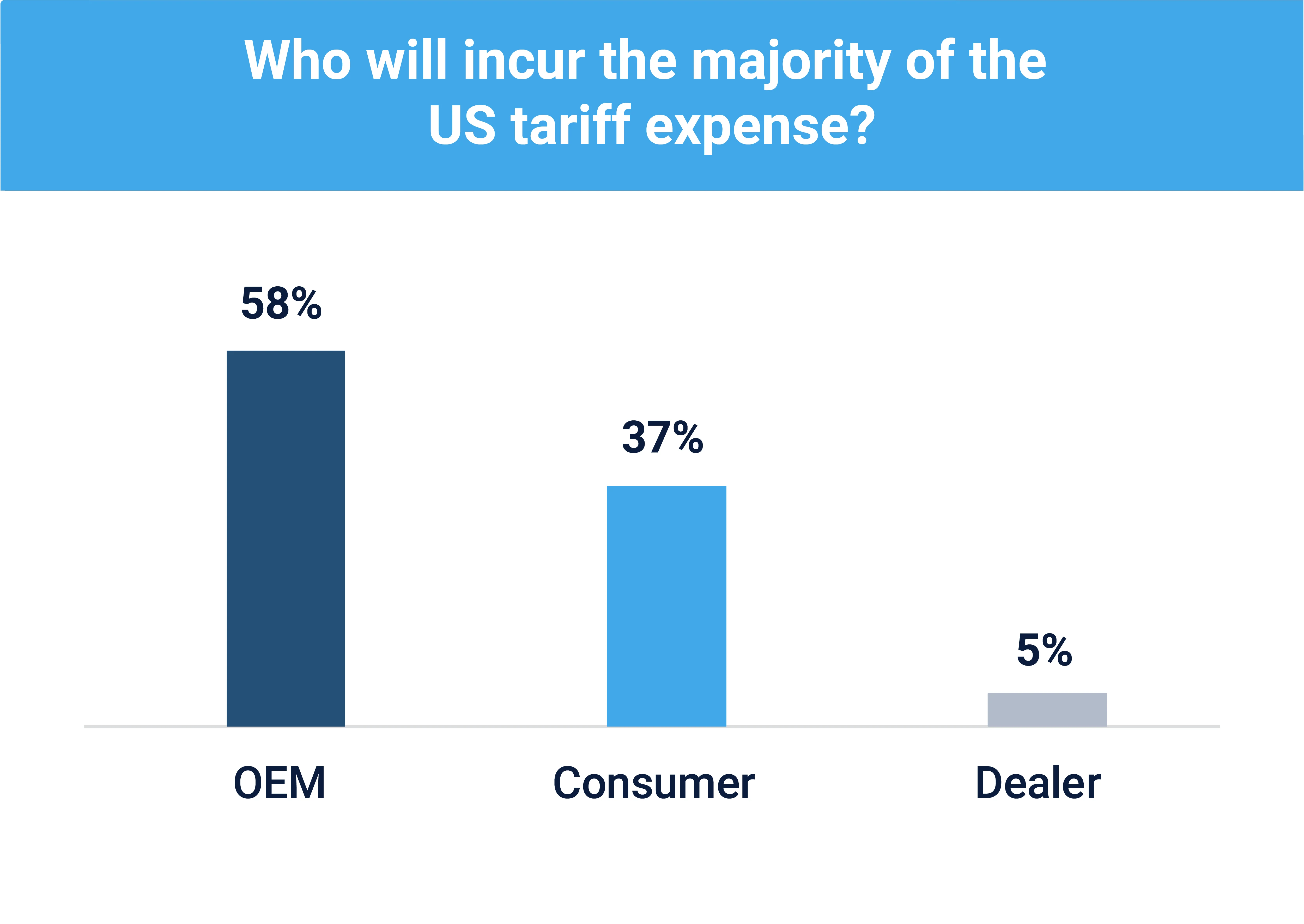

Kerrigan Advisors asked OEM executives who they expect to incur the majority of the US tariff expense. A majority (58%) believe OEMs themselves will bear the lion’s share of the cost, while 37% expect consumers to carry the burden. Notably, just 5% expect dealers to be the primary absorbers of tariff expenses. While this suggests OEMs do not intend to pass the bulk of tariff costs directly on to their dealer networks, it carries important implications for new vehicle sales. OEMs absorbing these costs are likely to scale back consumer incentives that support retail demand, while the portion of the tariff burden passed through to consumers will further strain new vehicle affordability in an already tight market — a dynamic that explains the softening vehicle sales outlook noted above.

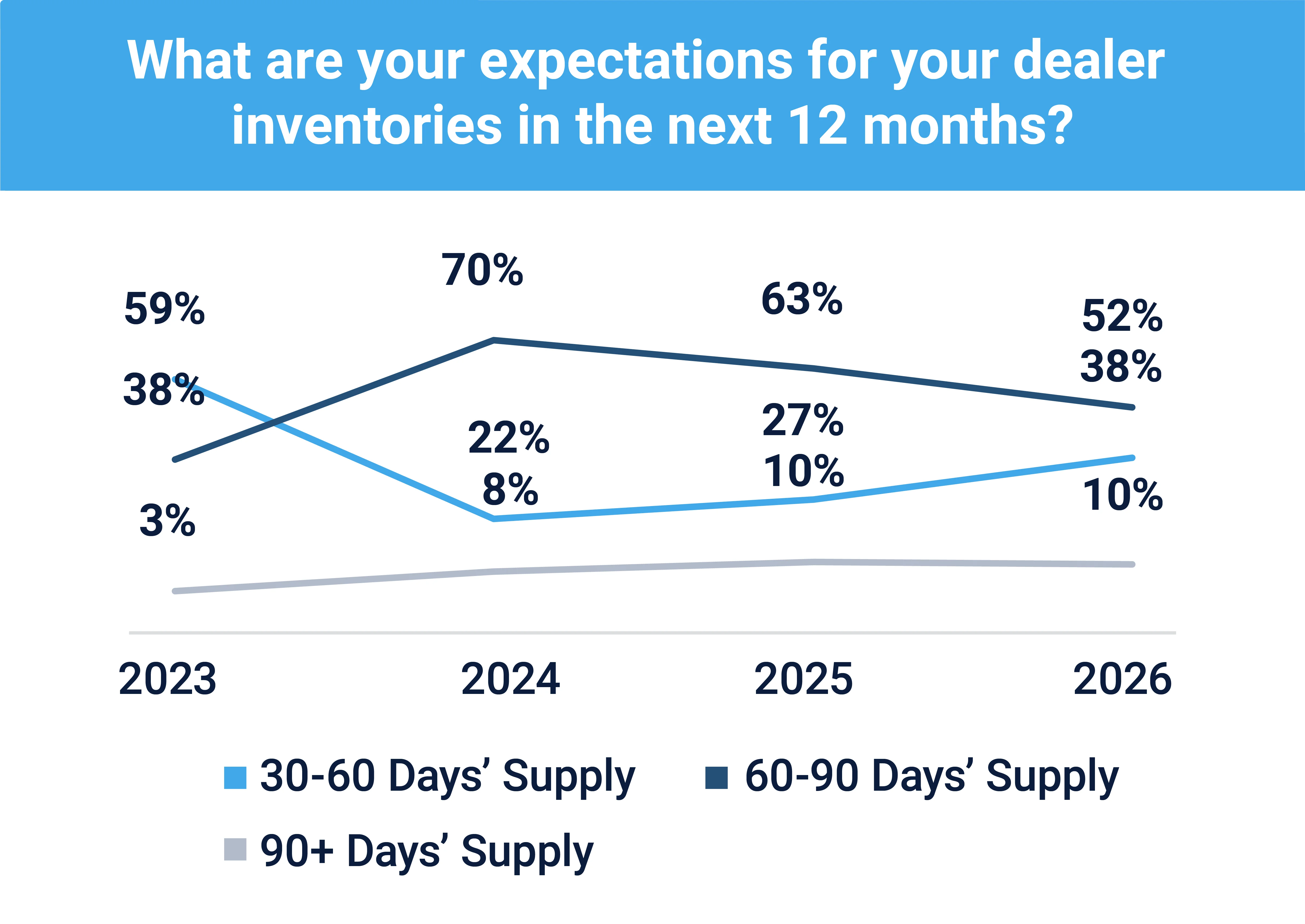

The survey results also indicate OEM expectations for dealer inventory levels continue to normalize toward healthier ranges. 38% of respondents expect a 30–60 days’ supply over the next 12 months, up 11 percentage points from 27% in 2025, while 52% project a 60–90 days’ supply and 10% anticipate a 90+ days’ supply, unchanged from the prior year. The shift toward the tighter 30–60 day range reflects OEMs’ more disciplined approach to production, particularly as EV production declines, and supports a more stable new vehicle margin environment.

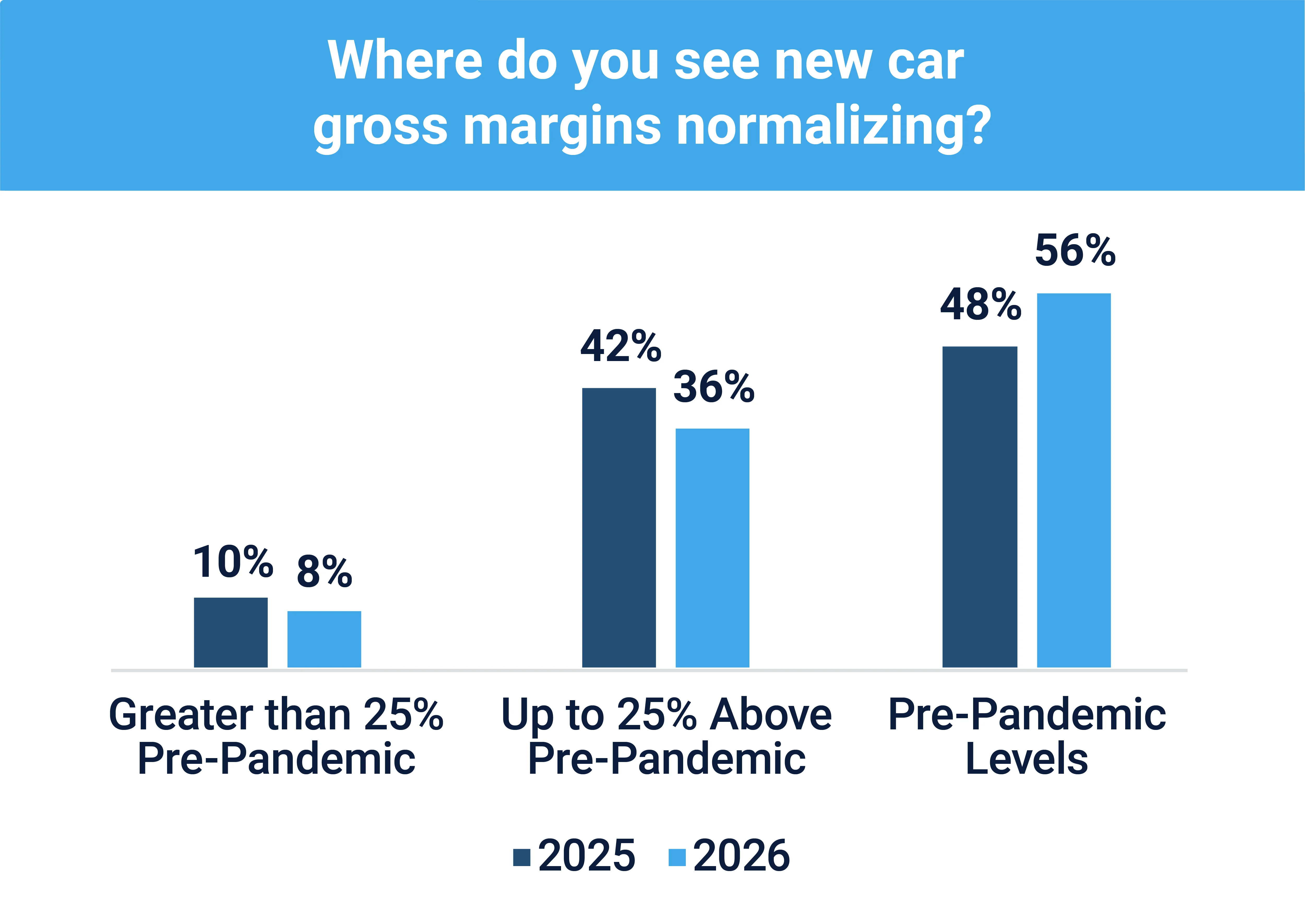

Even with a tighter inventory outlook, a rising majority (56%) now expect new vehicle gross margins to normalize back toward pre-pandemic levels, up eight percentage points from 48% in 2025, while 36% expect margins to settle up to 25% above pre-pandemic averages and 8% more than 25% above. Critically, this normalization in percentage terms does not signal a return to pre-pandemic profitability. With average new vehicle prices now roughly 30% above pre-Covid levels, even a normalized margin percentage translates into materially higher gross profit per vehicle on an absolute dollar basis — meaning dealers’ new vehicle profitability is likely to remain well above historical norms.

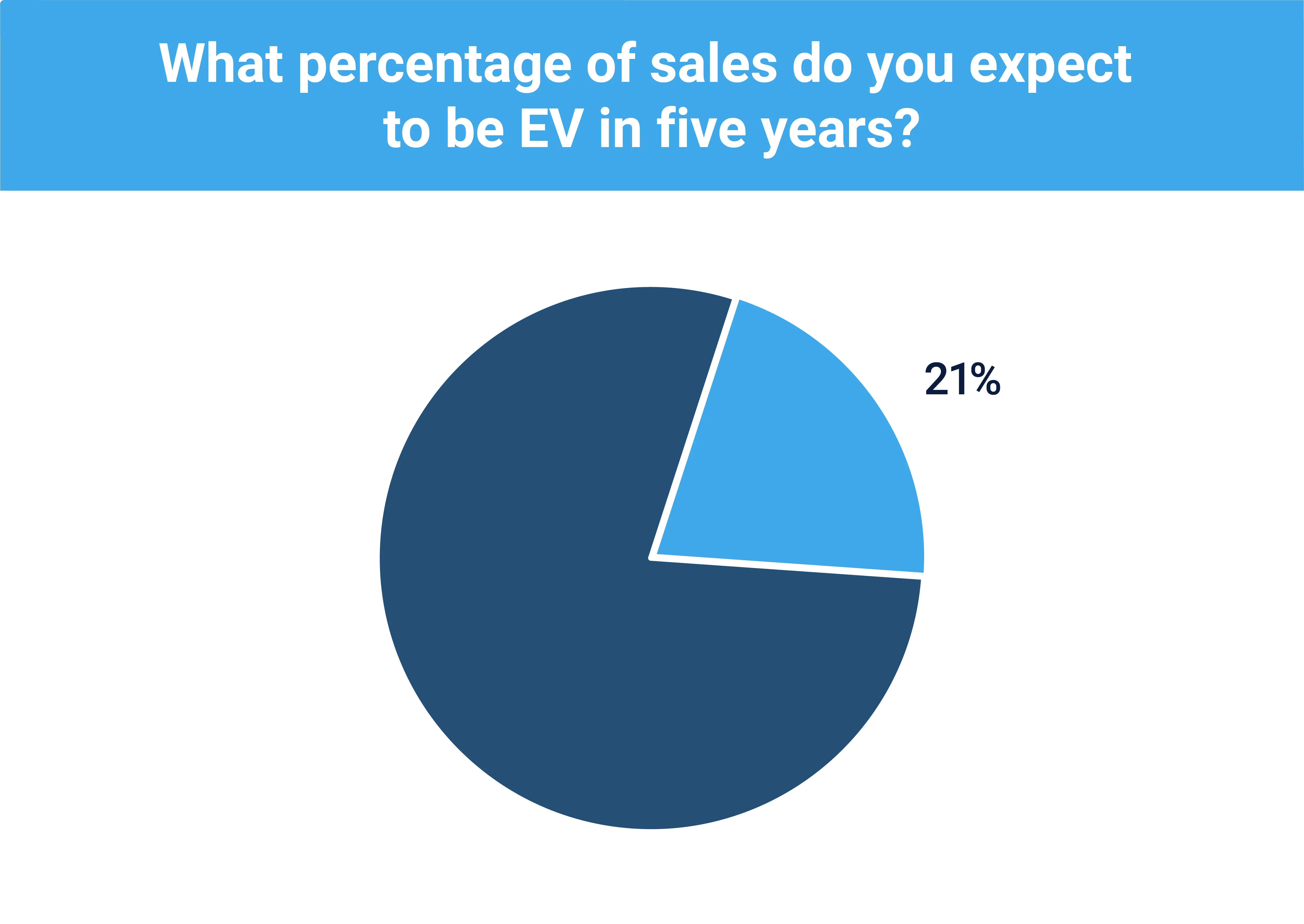

Kerrigan Advisors also queried OEM executives regarding EV adoption in the US auto retail marketplace. This year, executives were asked to project the share of their sales they expect to be electric within five years. On average, OEM executives expect EVs to represent 21% of sales in five years, a rate that is more than double EV market share in the US (~8% in 2025). That projection is striking given the year's sharp pullback in policy support, as both the federal EV tax credit and CARB EV mandate were eliminated. Even so, OEMs are not retreating from electrification despite tepid consumer demand and continue to project meaningful long-term growth in the segment, likely underpinned by the tens of billions of dollars they have already invested in EV development and production capacity over the past five years.

Perspective on OEM-Dealer Relations

This year’s survey again questioned OEM executives about their perspective on the franchise system and their evolving relationships with dealers.

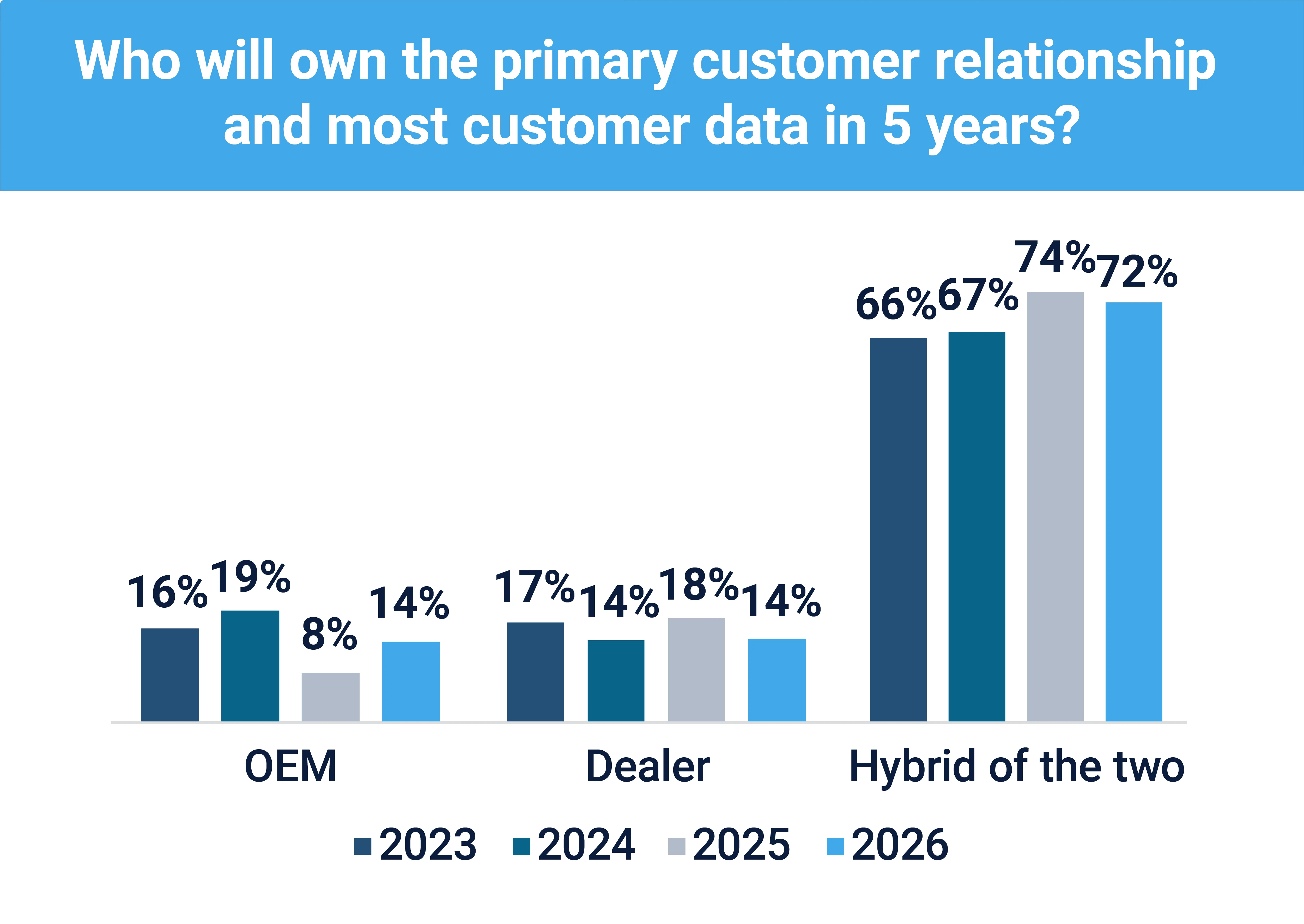

Importantly, OEMs continue to accept that the dealer will play a central role in managing the customer relationship and data over the next five years, either alone (14%) or together with the OEM (72%). However, the share of those who expect the OEM to be the exclusive owner of the customer relationship, while at a modest level overall, rose sharply from 2025, up six percentage points, though it remains lower than levels in 2023 and 2024.

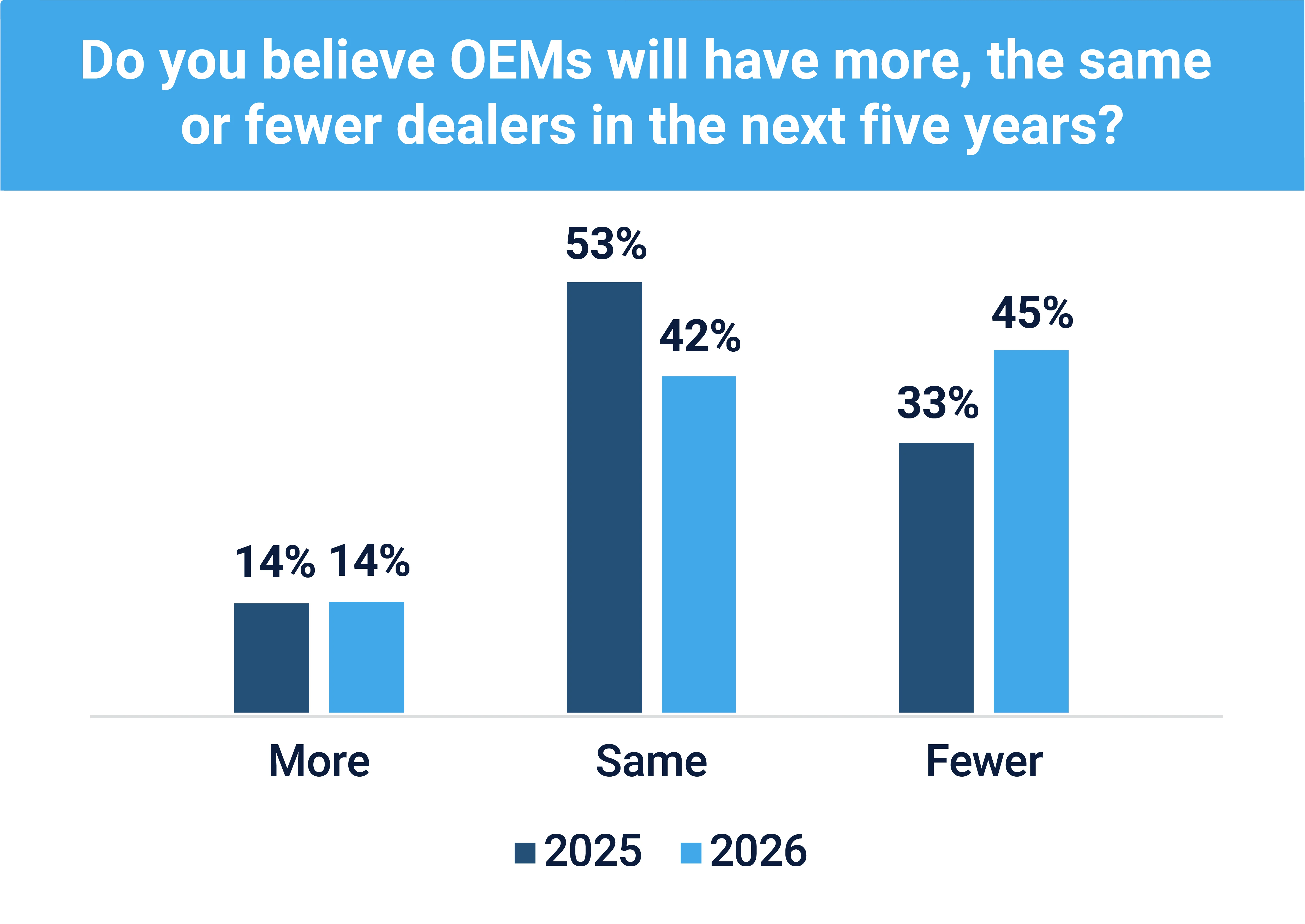

While OEMs largely accept the dealer’s critical role with the customer, a growing share are seeking to reduce the number of dealers in their networks. A notable 45% of OEM executives expect to have fewer dealers in their network in the next five years, a 12 percentage point increase from 33% in 2025, while 42% expect their network to remain the same size and 14% expect it to grow. This view reflects a continuation of the industry's long-term consolidation trajectory, with buy/sell activity now pacing at roughly double its pre-pandemic level and OEMs’ increasingly demonstrating their bias toward fewer larger dealers representing their brands.

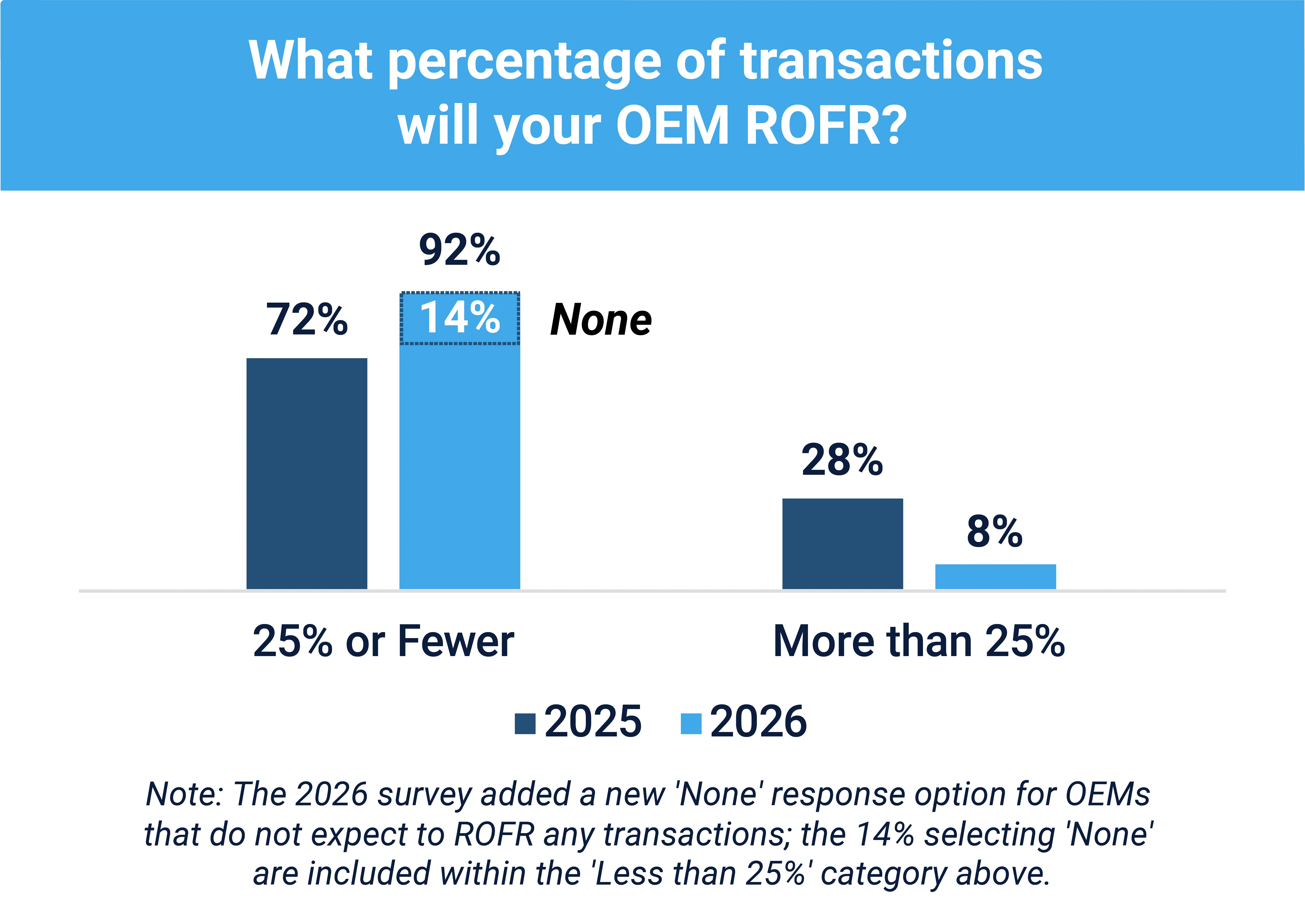

Even as OEMs express greater intent to consolidate their networks, their planned use of the right of first refusal (“ROFR”) has declined markedly. Just 8% plan to ROFR more than a quarter of transactions — down sharply from 28% in 2025. The remaining share includes 78% of executives who expect to ROFR less than 25% of their transactions and 14% who do not intend to ROFR any transactions (a new response option to the 2026 survey). This improvement from 2025 suggests OEMs are growing more content with market driven consolidation, as the dealer body continues to shift toward fewer and better-capitalized groups.

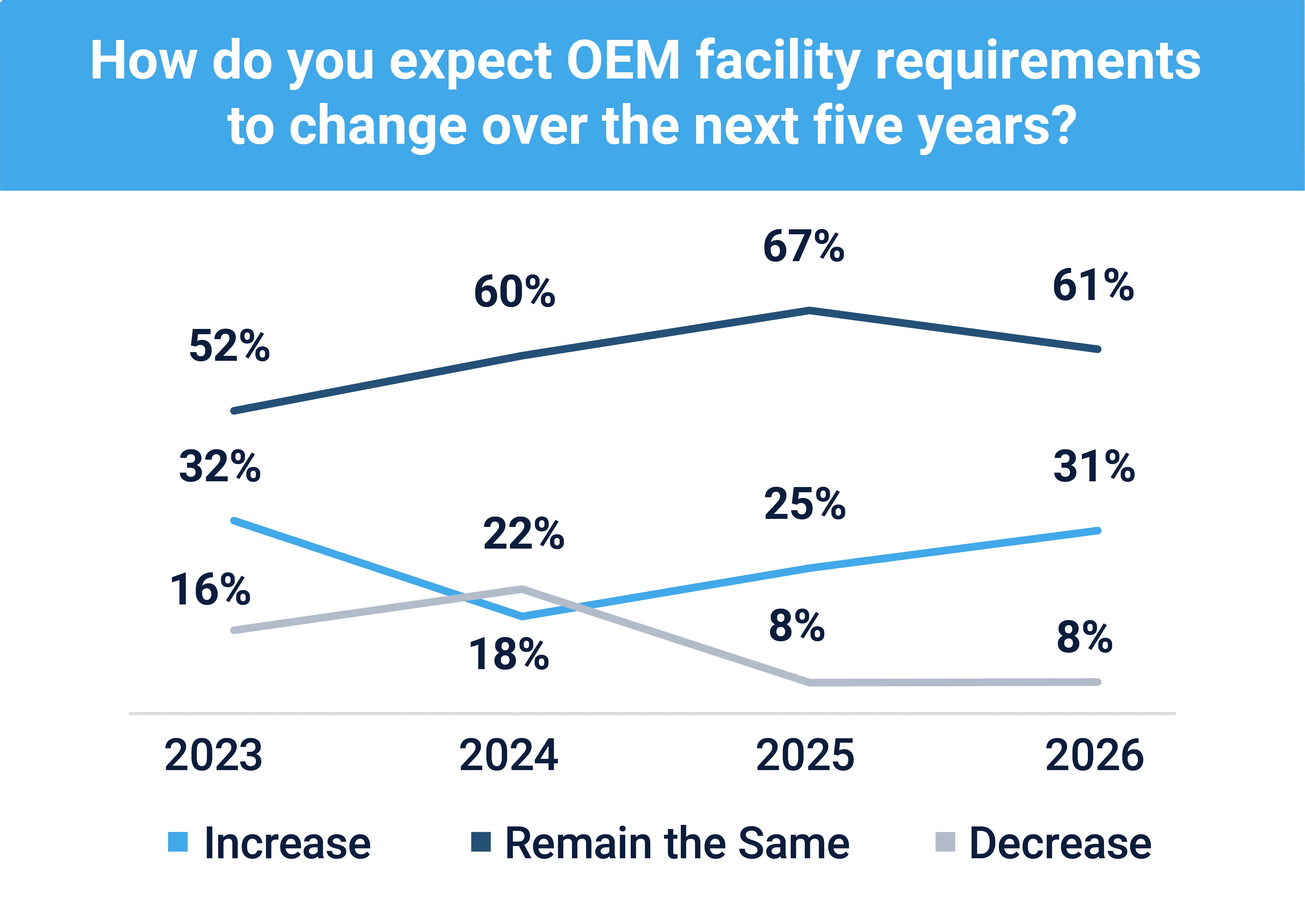

The survey results also demonstrate that OEMs continue to demand more of their dealers with respect to facility requirements. 31% of respondents project an increase in facility requirements over the next five years, up six percentage points from 25% in 2025, while 61% expect today’s already high standards to remain in place and just 8% anticipate a decrease. Increasingly, Kerigan Advisors sees these image investment requirements prompting dealers to reassess their capital allocation. In a growing number of cases, dealers are choosing to divest dealerships whose facility investments yield a low or negative return, making rising facility expenses a meaningful driver of dealers' decisions to sell.

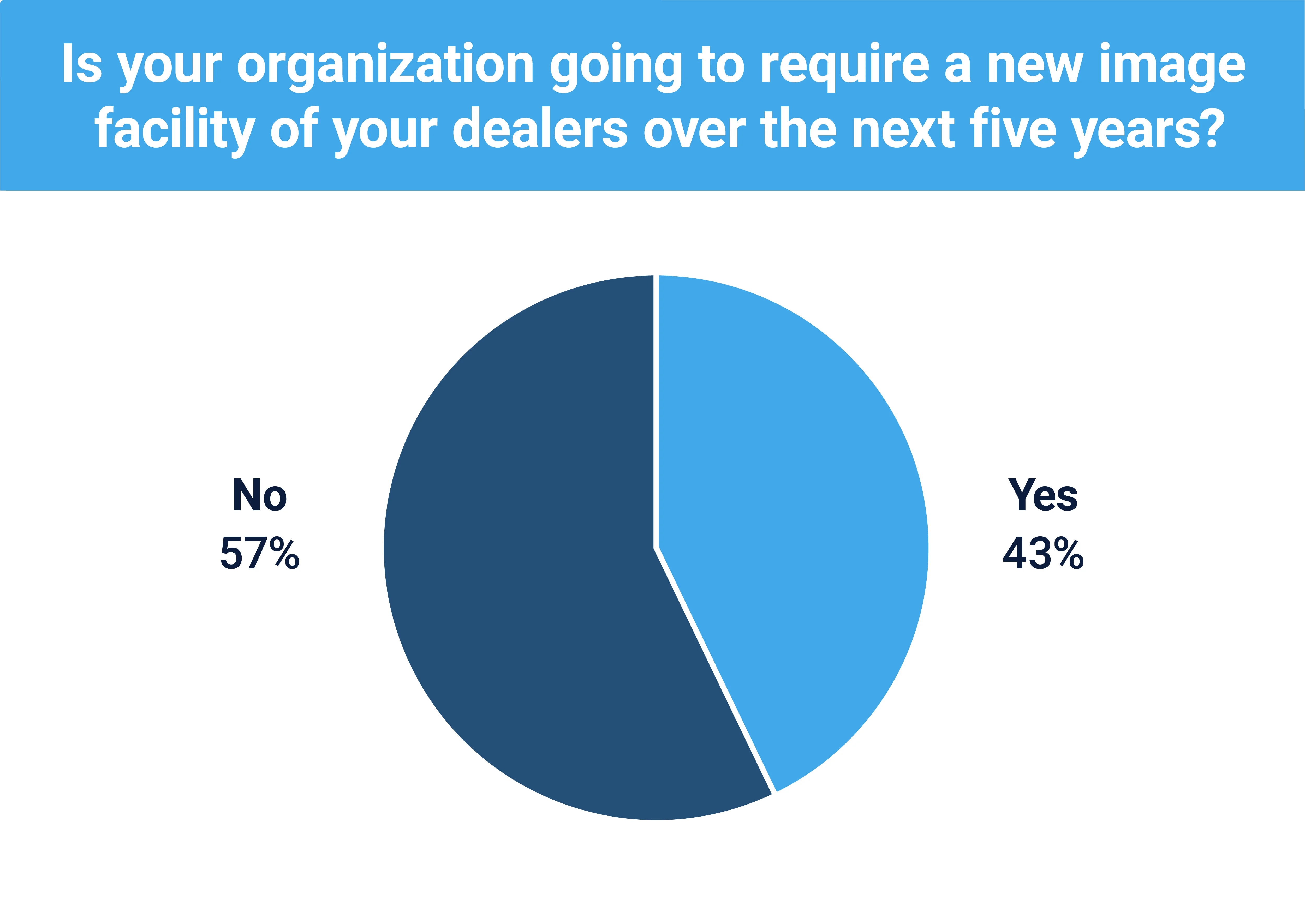

Reinforcing this trend, Kerrigan Advisors asked OEM executives whether their organization will require a new image facility of their dealers over the next five years. 43% of respondents indicated they will, underscoring the rising capital demands placed on dealers and the pressure these requirements create, particularly for smaller operators with more capital constraints.

The 2026 Kerrigan OEM Survey points to a highly active buy/sell market over the next 12 months and continued strength in today's dealership valuations. OEMs are steering toward a more concentrated network of fewer, larger and well-capitalized dealers who are best positioned to capture the higher dealership profits expected from AI adoption and to fund the escalating facility investments they increasingly demand of dealers. Taken together, these results are a clear endorsement of the franchise retail model's critical role in US auto retail, with an equally clear expectation that its future belongs to the industry's best-capitalized and largest operators.

The data for the 2026 Kerrigan OEM Survey was gathered from Kerrigan Advisors’ annual survey of automotive OEM executives in conjunction with the issuance of The Blue Sky Report®. The survey is based on 150+ responses from OEM executives in Kerrigan Advisors’ proprietary database from December 2025 to June 2026.

Contact us to learn more about Kerrigan Advisors’ premier advisory services for dealers and investors.

All of our conversations are 100% confidential.