Kerrigan Advisors’ seventh annual Dealer Survey is a unique industry resource designed to assess dealer sentiment on the future value of their businesses, franchise earnings and valuation expectations. The survey also explores the most pressing issues currently impacting auto retail, including artificial intelligence and tariffs, and captures dealer perspectives on each franchise—measuring trust levels, acquisition interest and blue sky trends.

Kerrigan Advisors’ seventh annual Dealer Survey is a unique industry resource designed to assess dealer sentiment on the future value of their businesses, franchise earnings and valuation expectations. The survey also explores the most pressing issues currently impacting auto retail, including artificial intelligence and tariffs, and captures dealer perspectives on each franchise—measuring trust levels, acquisition interest and blue sky trends.

Kerrigan Advisors’ annual Dealer Survey is designed to gauge dealer sentiment on the future value of their businesses, franchise earnings and valuation expectations, as well as perspectives on their trust levels with each OEM.

The results of this year’s survey show some signs of increased optimism amongst the US dealer body. 29% of dealers surveyed have a positive outlook for their business over the next 12 months, relative to 26% having a negative view. Overall, steady state seems to be the overriding vantage point for 2026, with 46% reporting no change in their outlook for the business over the next 12 months.

Similar to their view on the business outlook, the majority of dealers (59%) expect no change to valuations in 2026. That said, 24% of dealers expect valuations to increase in 2026, a 41% improvement over last year, while only 16% expect a decline, a 52% reduction from last year. These results mark the first improvement in valuation expectations since 2021 and reflect the first time since that year that more dealers expect an increase rather than a decrease in valuation (24% increase versus 16% decrease). This positive reversal is consistent with Kerrigan Advisors’ Blue Sky Reports where we project 2024 to be the trough in average blue sky values, with positive increases expected in 2026.

The improvement in valuation expectations is consistent with dealers’ more optimistic views of profitability for 2026. As compared to last year, more dealers now project an increase rather than a decrease in earnings. 32% of dealers surveyed project profits will rise in 2026, a 129% increase from last year. This is a significant turnaround from 2024 when 43% were expecting a profit decrease. The improved earnings outlook is consistent with the expectations of higher valuations in 2026 and a more constructive industry outlook.

Consistent with dealers' renewed optimism, more dealers are seeking to expand their group with the addition of at least one dealership in 2026. Most dealers are focused on tuck-in acquisitions in their existing markets, with the majority of transactions completed by dealers who already have a presence in the market in which they are acquiring. 32% of dealers surveyed plan to add one dealership to their group over the next 12 months, up six percentage points from 2022’s low. That said, fewer dealers are looking to add groups to their business with only 14% planning to add two or more dealerships, down from 31% in 2021. These results are consistent with the decline in multi-dealership transactions witnessed in 2025 when less than 20% of transactions included more than one franchise.

Kerrigan Advisors also asked dealers which franchises they are seeking to add to their enterprise in 2026. The results are consistent with Kerrigan Advisors’ proprietary Buyer Network of more than 1,400 dealership buyers nationwide.

Toyota and Lexus are by far the most requested brands by buyers consistent with this year’s survey results. The OEM’s measured approach to network size, EV strategy and judicious inventory management remain highly attractive to buyers, making the franchises the most requested in their respective categories. Notably, the ranking of buyers’ franchise preferences were unchanged from 2024, with the exception of Cadillac moving ahead of JLR and Acura moving ahead of Volvo.

Kerrigan Advisors also quired dealers regarding the impact of US tariffs on their businesses. Interestingly, 44% of dealers reported no impact on their business as a result of tariffs. That said, tariffs are having some effect on dealers’ plans to invest in their business, with more looking to add dealerships as a result of tariffs (16%) rather than sell dealerships (3%), an eight-to-one ratio. Even with this increased interest in growth, fewer dealers are planning to increase their capital investments as a result of tariffs and fewer are planning to increase headcount, demonstrating some investment trepidation due to the current US tariff policy.

Likewise, fewer dealers are seeking to increase their new vehicle inventory and are rather focused on expanding their non-tariffed used inventories.

Consistent with dealers’ disinterest in making capital investments, a significant percentage of dealers surveyed (42%) expect real estate and property investments required by the OEM, including EV infrastructure, will have a negative impact on future profits. Only 13% project an improvement in earnings as a result of these investments.

Kerrigan Advisors also surveyed dealers regarding their utilization of artificial intelligence (“AI”) in their dealership operations. Not surprisingly, 43% of dealers are already deploying AI solutions in their business and 47% have plans to do so. Only 10% do not use AI or have any plans to use AI. Based on these results, Kerrigan Advisors expects AI to have a meaningful impact on industry results in 2026 and beyond.

Note: These results reflect the view of the 525+ dealers surveyed, regardless of a dealer’s specific franchise ownership.

Consistent with last year, the majority of dealers surveyed believe individual franchises will either remain the same in value or increase over the next 12 months. That said, the variability amongst franchises in valuation expectations continued to diverge, primarily driven by profitability projections. Of note this year, every domestic franchise saw an improvement in their valuation expectations for 2026, with each seeing a rise in those projecting an increase in valuation (102% improvement on average). By contrast, all imports, both luxury and non-luxury, saw a decline in their upside valuation expectations for 2026. These results may be a product of the Trump administration’s economic policies that favor US manufacturers.

Highest Expected Valuation Gains and Least Likely to Decline in Value:

Toyota, Lexus, Honda, Kia, Subaru and Chevrolet

Over 20% of surveyed dealers expect these six franchises to increase in value in the next 12 months. This is the first time Chevrolet has ranked 6th amongst all franchises, a dramatic improvement from last year when the franchise ranked 12th. Also of note, Hyundai, which ranked 2nd most expected to increase in value in 2024, now ranks below Chevrolet and far below its sister franchise, Kia, which has remained amongst the top performers now for four years. 2025 is also the second year in a row where the top performers in this category included only one luxury franchise (Lexus) with BMW, Porsche and Mercedes ranking 7th, 8th and 9th, respectively.

Highest Expected Valuation Declines:

Infiniti, Nissan, Volvo, Volkswagen and CJDR

Over 50% of surveyed dealers expect these franchises to decline in value in the next 12 months. Notably, while CJDR remains on this list, the franchise saw the biggest improvement of any franchise in valuation projections for 2026, improving 10 percentage points in its expectations of an increase and 26 percentage points in its projected decline. Also of note, Nissan and Volkswagen have had the steepest peak to trough declines in this category, demonstrating momentum in dealer’s negative views of these franchises.

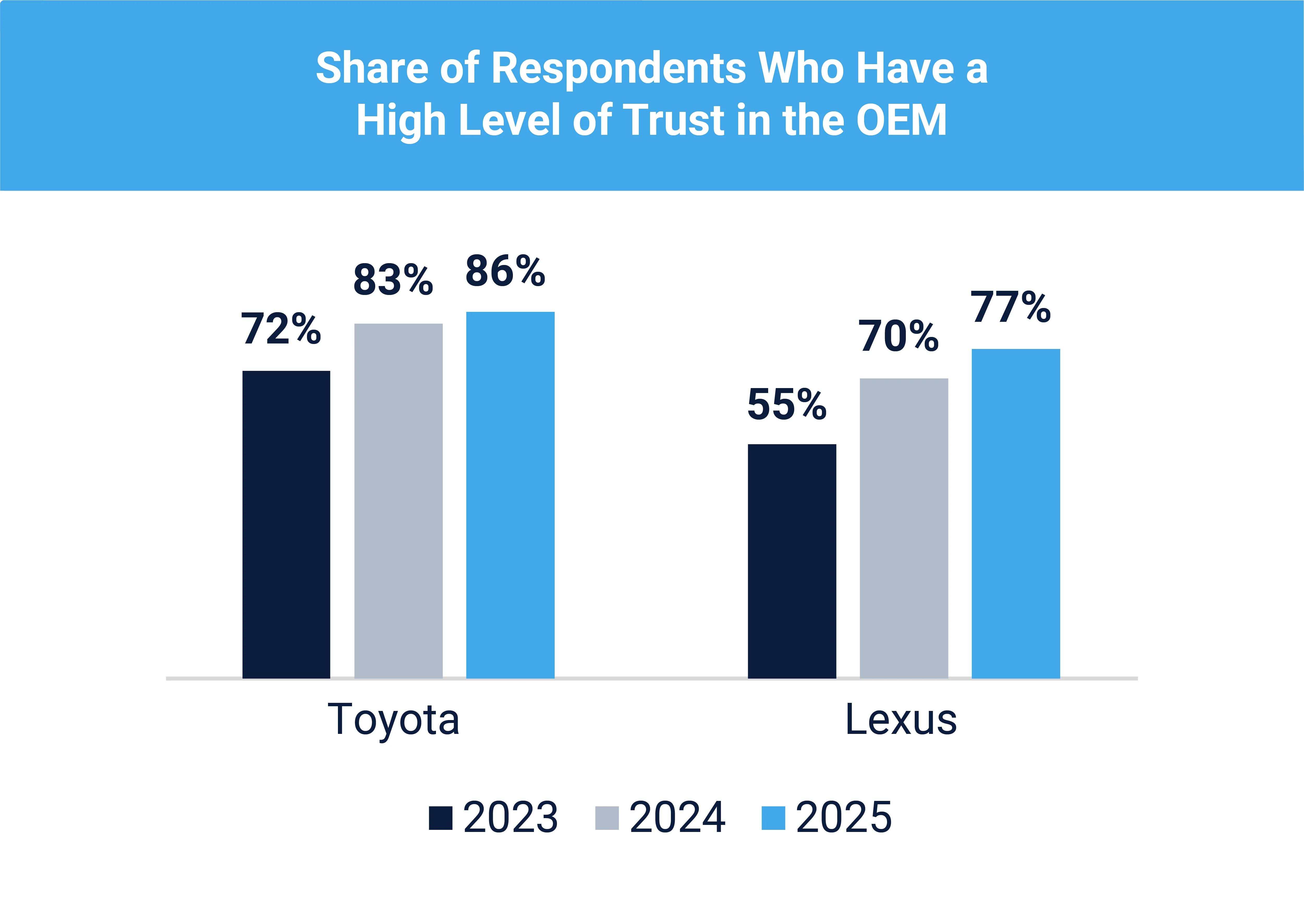

For the third year in a row, Kerrigan Advisors queried dealers about their trust level in each franchise. Toyota again received the top results by far, with 86% of dealers indicating they had a high level of trust in the franchise, 3.3x higher than the survey average (25%). By contrast, 64% of dealers reported they had no trust in Nissan, consistent with the expectation of a decline in future Nissan valuation.

The most trusted franchises are those who are least likely to see a decline in valuation, while the least trusted are largely the franchises most expected to decline in valuation.

Notable improvements were made by certain franchises in the trust category this year. Specifically, Chevrolet, Buick GMC and CJDR saw the largest improvements in dealers who had a high level of trust in the franchises, while Cadillac, Ford and CDJR reported the largest improvement in dealers who had no trust in the franchises, down greater than 8 percentage points for each franchise. These results are consistent with the valuation improvement expectations in for all of the domestics for 2026.

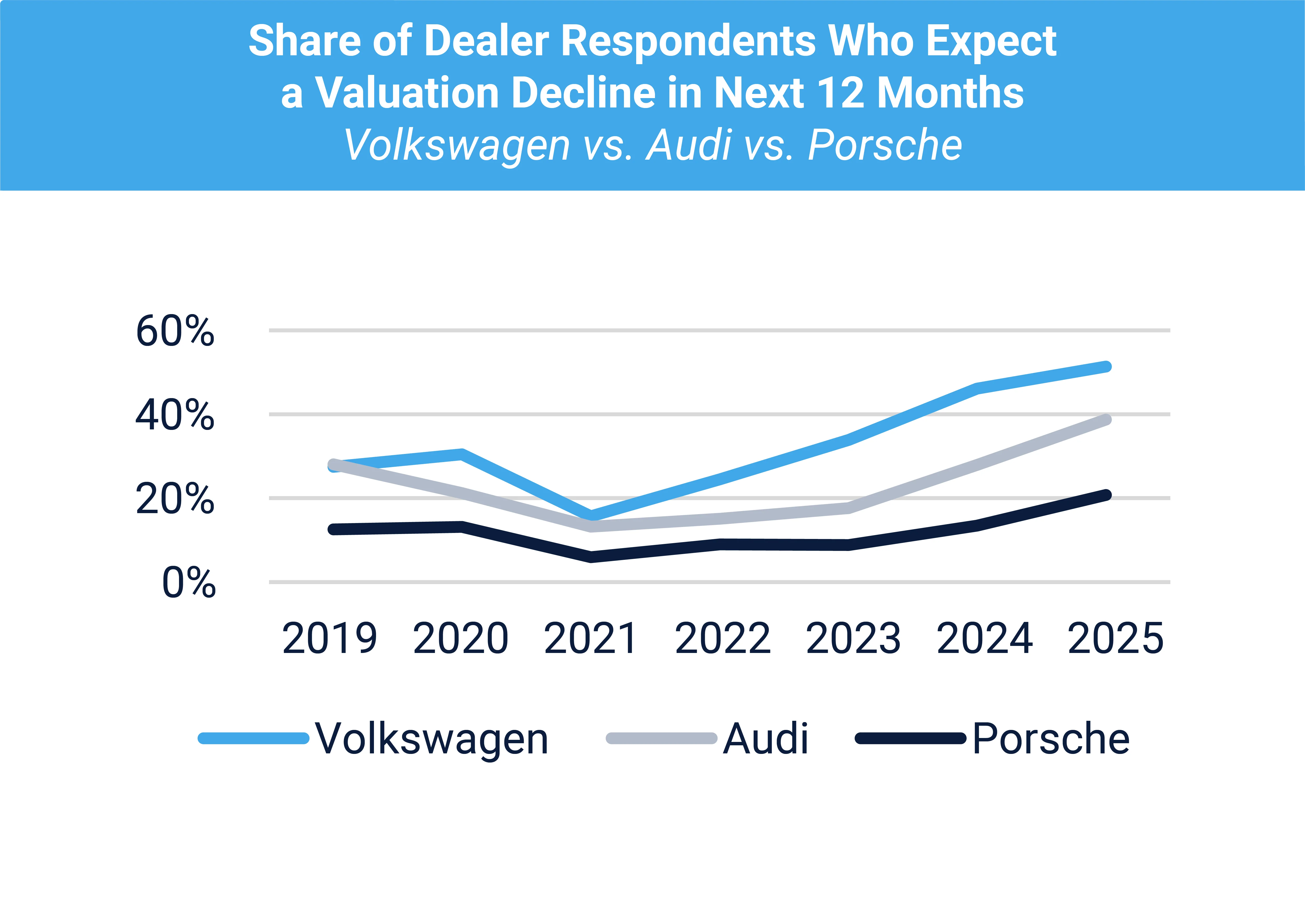

While the domestics saw improvements, Volkswagen saw the largest percentage point declines. Specifically, Volkswagen and Audi’s No Trust rating increased 11 percentage points compared to last year and Porsche’s High Level of Trust rating declined 8 percentage points.

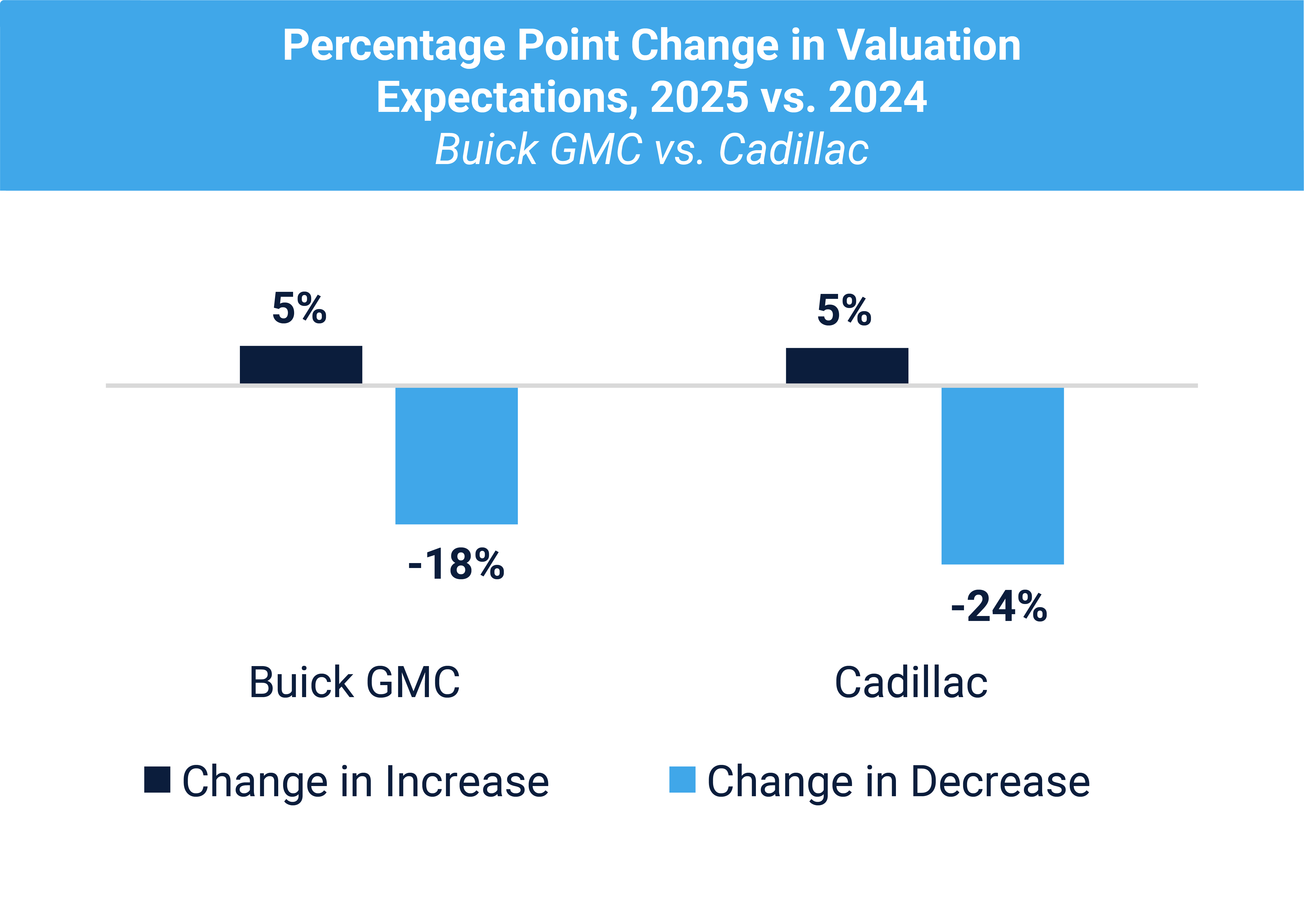

General Motors

General Motors leads the way in this year’s survey with the most improvements compared to last year. Specifically, Chevrolet was one of the top performers, ranking 6th in expected valuation increases, up from last year’s 12th position – the largest ranking improvement of any franchise. In fact, Chevrolet surpassed Hyundai for the first time in valuation expectations, a dramatic turnaround for both brands.

In addition, Buick GMC and Cadillac also saw strong results in this year’s survey. The brands rebounded from 2024’s low, seeing one of the strongest improvements of any franchises in the survey. Notably, both franchises also saw dramatic increases in trust levels amongst the dealer body. Cadillac also moved ahead of JLR in terms of luxury franchises buyers are seeking.

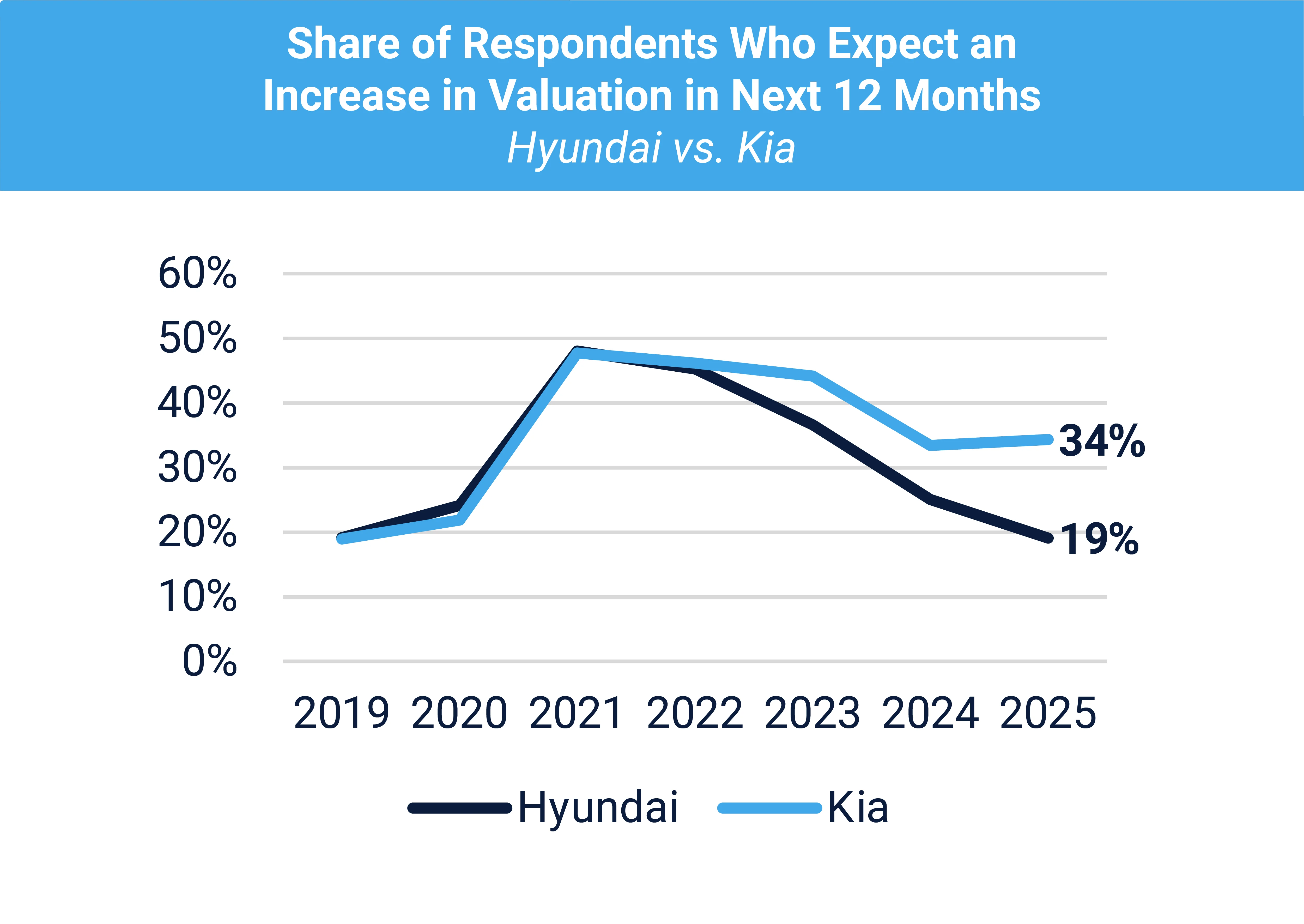

Hyundai

Hyundai’s results diverged significantly between its namesake franchise and Kia. While Hyundai continued to see a deterioration in its valuation expectations and trust levels, Kia remained one of the top franchises in valuation increase expectations for 2026, ranking 3rd this year. Kia’s high level of trust amongst the dealer body is 27%, more than double that of Hyundai at 13%. Only 19% of dealers surveyed expect the Hyundai franchise to increase in value in 2026, in contrast to Kia’s 34%. Also, 24% of buyers are seeking Kia franchises relative to Hyundai’s 17%.

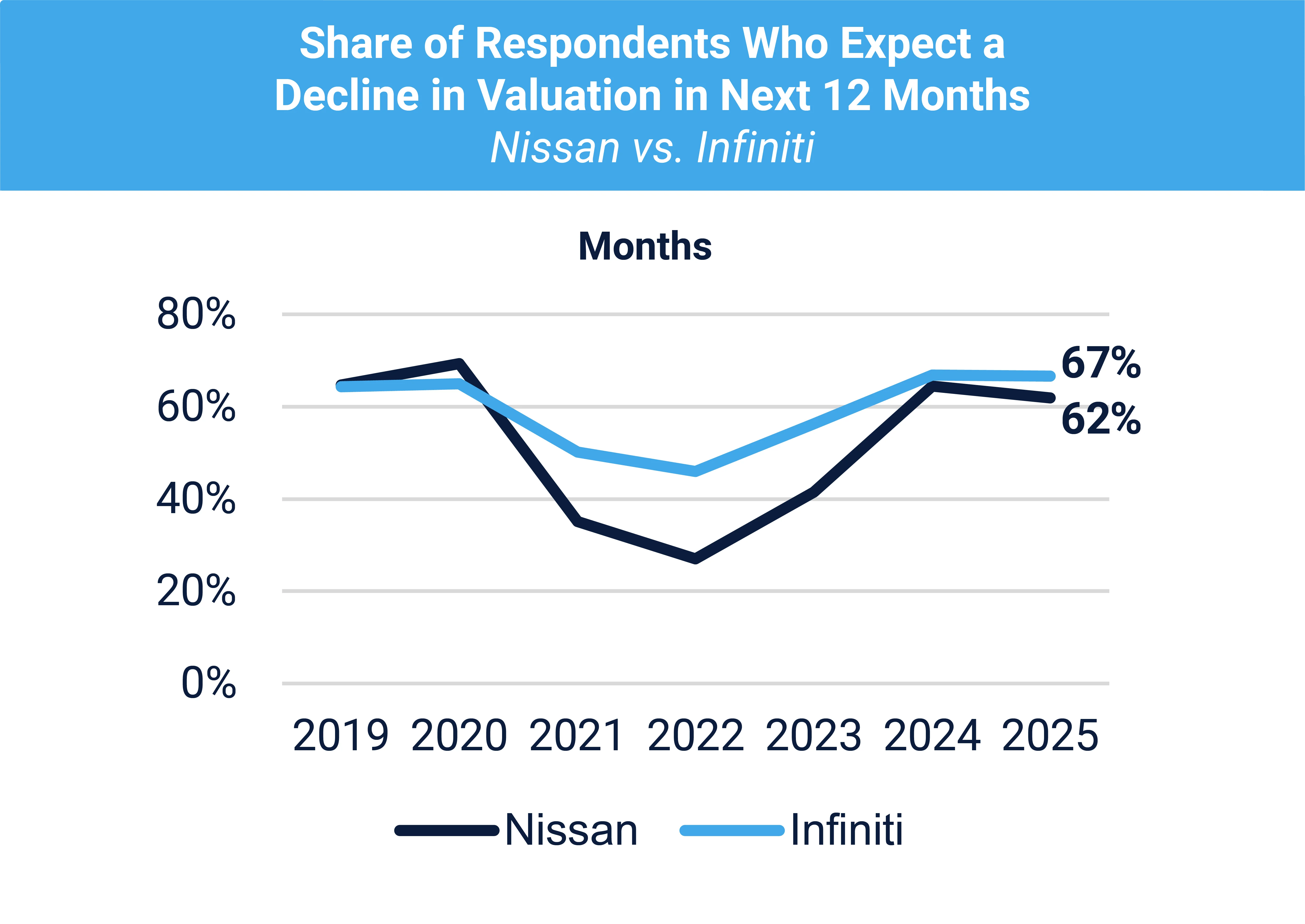

Nissan

Nissan continued its poor performance from last year, both for its namesake brand and Infiniti. Both franchises are the most expected to decline in value in 2026, with greater than 62% of dealers surveyed expecting a decline, the highest result in this year’s survey. Also, the franchises are the least trusted in the industry, with greater than 61% having no trust in the OEM. Only 6% of buyers are seeking to add a Nissan franchise and just 1% are interested in an Infiniti franchise, the lowest ranking of all franchises.

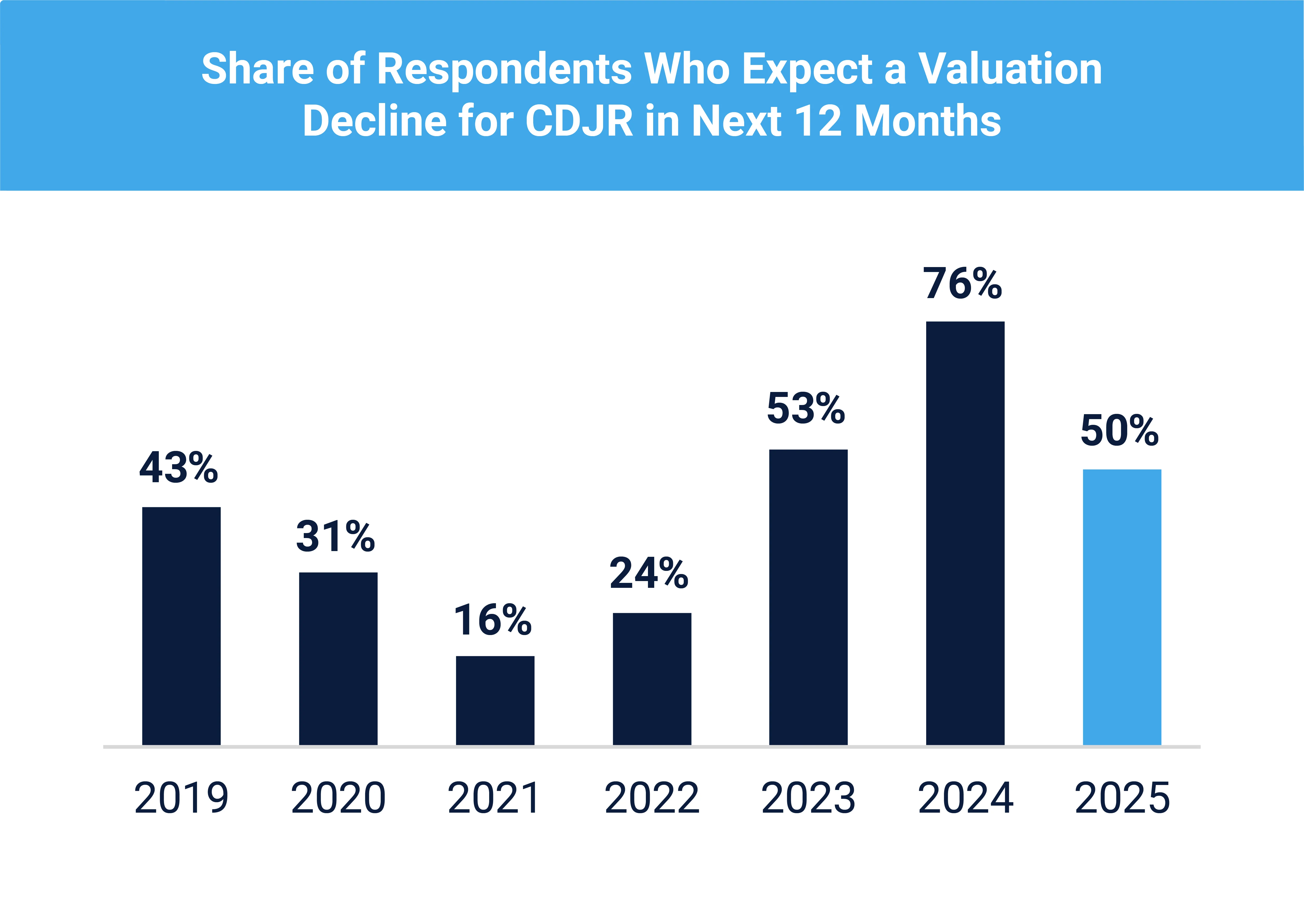

Stellantis

Stellantis saw the greatest improvement of any OEM in its survey results this year related to valuation. The percentage of dealers surveyed expecting a decline in CJDR’s value declined by 26 percentage points from last year, the largest improvement of any franchise. Also, those expecting an improvement in valuation rose 10 percentage points to 15%. That said, the trust level in the franchise remains amongst the lowest in the industry (2nd lowest behind Nissan), with 64% of dealers surveyed having no trust in the franchise. The OEM has a long way to go to return to its 2021 valuation expectations when only 16% of dealers expected a decline in value.

Toyota

Toyota continues to outshine all its competition, leading in every category of the survey. Both its namesake franchise and Lexus reported the highest valuation increase expectations, the most trust and the highest buyer demand. Toyota and Lexus’ high level of trust is now greater than 3x higher than the industry average and its valuation increase expectations is more than 2.25x higher than industry average.

Volkswagen

Volkswagen Group experienced a dramatic decline in survey results this year. Specifically, Volkswagen, Audi and Porsche saw dramatic increases in dealers projecting a decline in valuation in 2026, with Porsche and Audi leading the industry in percentage point changes from last year and Volkswagen ranking 4th (Volkswagen: 7, Audi: 13 and Porsche: 11). In addition, nearly half of dealers surveyed have no trust in the Volkswagen brand (47%) and Volkswagen and Audi’s No Trust rating increased 11 and 8 percentage points, respectively, compared to last year and Porsche’s High Level of Trust rating declined 8 percentage points, the largest negative moves of any franchise.

The 2025 Kerrigan Dealer Survey results demonstrate the ever-changing auto retail environment and the fluidity of dealers’ perspectives regarding their OEMs. The majority of dealers project profits and valuations will remain at current levels or rise in 2026, with fewer dealers expecting declines. In this regard, 2025 appears to be a turning point for the industry and the beginning of an upward earnings and valuation period. A rising number of dealers seek to add at least one dealership to their group over the next 12 months, an indication of an overall positive industry outlook toward growth. That said, dealers have distinctly varying views on specific franchises, with certain OEMs eliciting a lack of trust and confidence, while others see valuation improvements, particularly the domestics. Based on these results, Kerrigan Advisors believes 2026 will be a robust year for buy/sell activity, with buyers seeking trusted brands and continuing to divest franchises they find more challenging.

The data for The Kerrigan Dealer Survey was gathered from Kerrigan Advisors’ seventh annual survey of auto dealers in conjunction with the issuance of The Blue Sky Report®. The Kerrigan Dealer Survey is based on 525+ anonymous responses from franchised auto dealers in Kerrigan Advisors’ proprietary dealer database. Responses were collected from June 2025 to November 2025.

The above testimonials may not be representative of the experience of other clients and should not be construed as a guarantee of future performance or success.

Contact us to learn more about Kerrigan Advisors’ premier advisory services for dealers and investors.

All of our conversations are 100% confidential.