While the number of US dealerships remains relatively stable at approximately 18,300 rooftops and the average dealer still owns less than three dealerships, the industry’s fragmentation is quite misleading because industry revenue is consolidating at a far more rapid pace than rooftops.

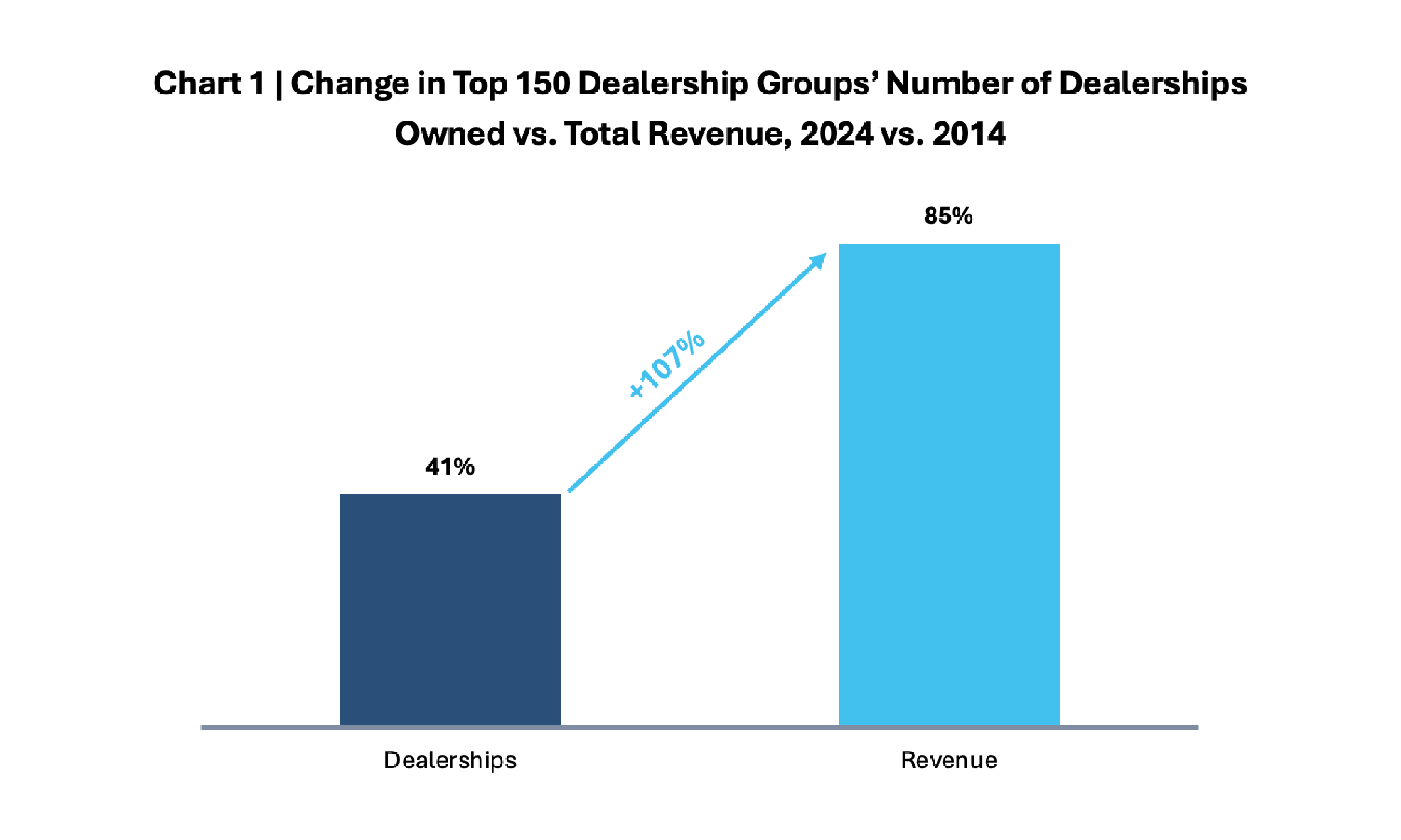

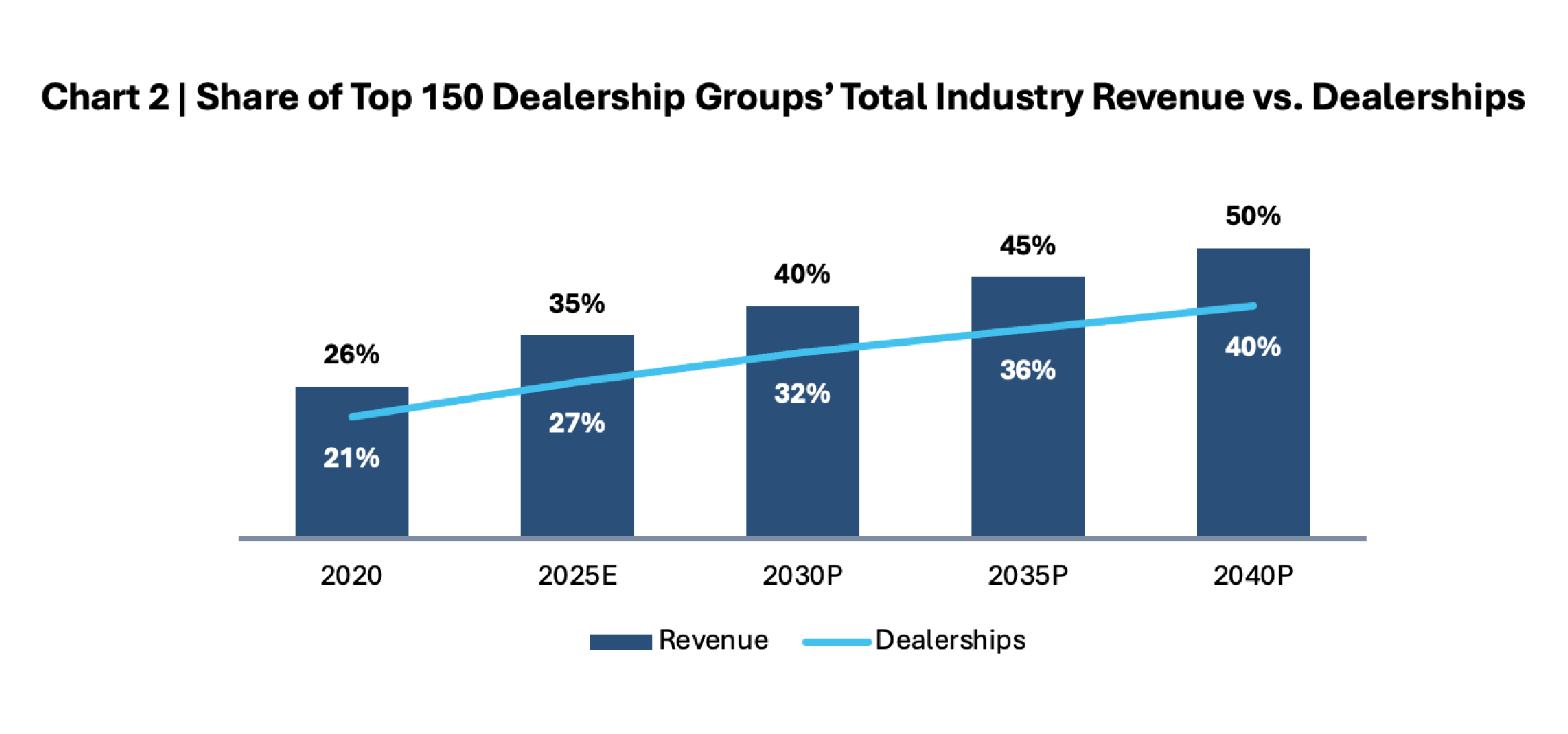

As an example, the Top 150 Dealership Groups (“Top 150”) are growing their revenue at a rate that is more than double their rooftop count (see Chart 1). Since 2014, the Top 150’s revenue increased by 85%, whereas rooftops rose by just 41%. At their current growth rates, the Top 150 are tracking to 50% of industry revenue market share and just 40% of rooftop market share by 2040 (see Chart 2). Increasingly, consolidator rooftop count is much less relevant than their total revenue growth.

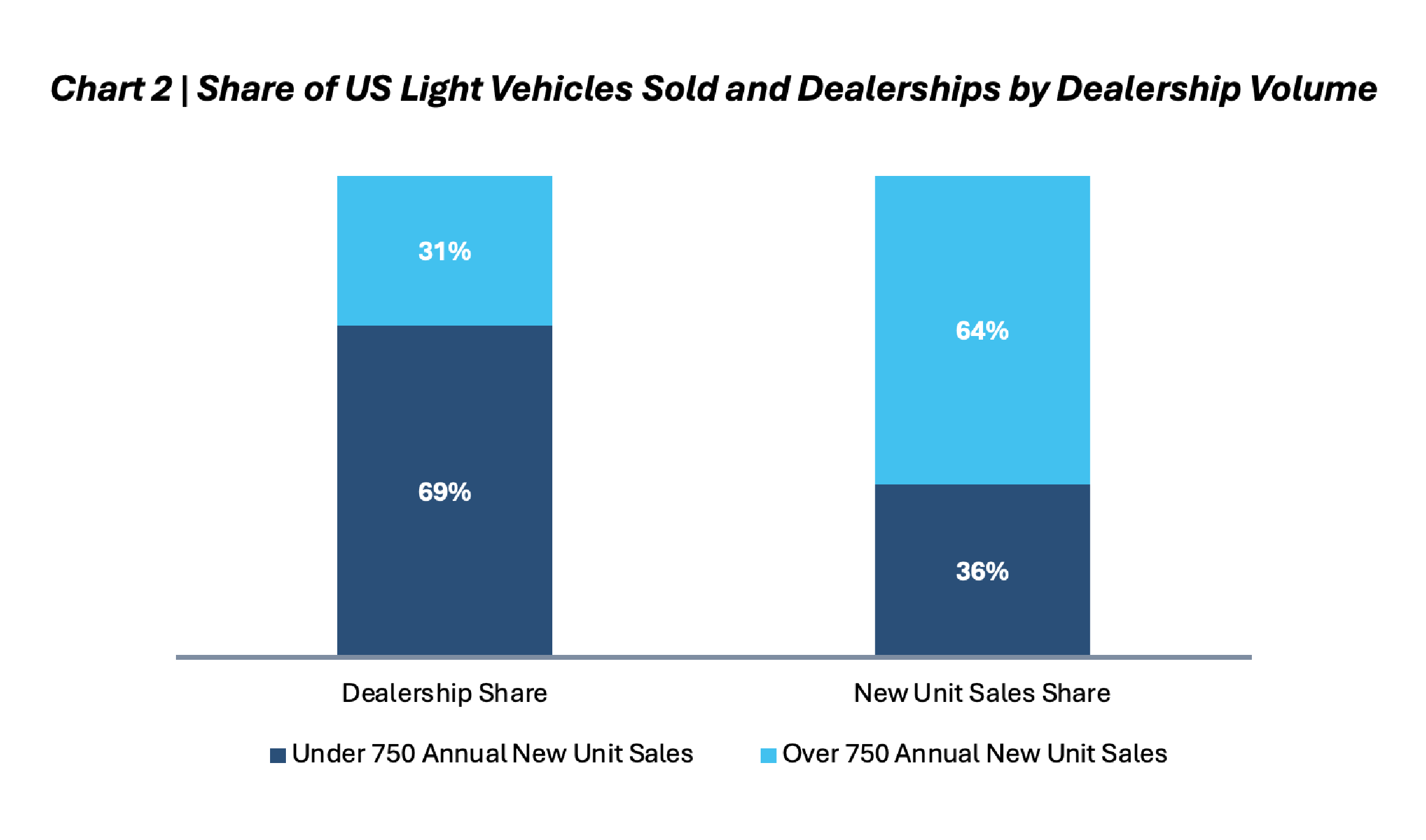

With industry revenue increasingly concentrated in the hands of fewer dealerships and dealership groups, scale on a top line basis is becoming a competitive advantage both on an enterprise and rooftop level. To highlight this point, Kerrigan Advisors estimates that 31% of the dealerships that retail more than 750 new units annually (approximately 5,310 rooftops) represent an estimated 64% of total new vehicle sales (see Chart 2). By contrast, the remaining 69% of dealerships (approximately 11,660 rooftops) account for just 36% of new vehicle sales. In other words, less than one-third of US rooftops generate more than two-thirds of new vehicle sales volume.

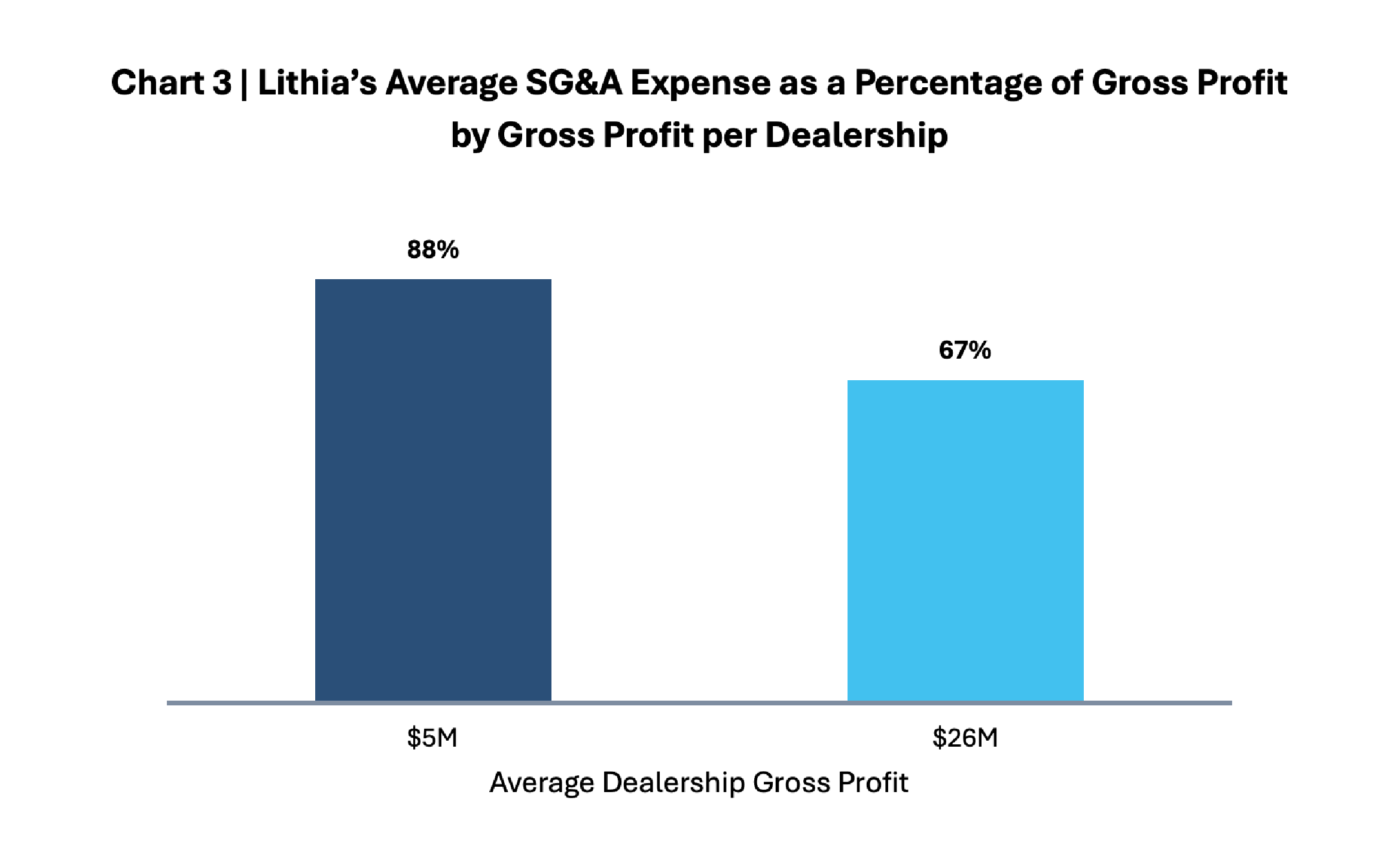

This imbalance underscores a structural shift within auto retail: throughput per rooftop is often the biggest driver of dealership profitability. Higher-volume dealerships benefit from superior fixed-cost absorption and greater service revenue given higher UIO counts. This leads to a lower relative cost structure and higher, consistent net-to-sales margins. As a result, revenue per location is often more relevant to group financial performance than pure rooftop count. Lithia noted this dynamic in its fourth quarter earnings presentation, where it discussed the desire to grow its pool of higher volume dealerships due to their more attractive cost structure (see Chart 3).

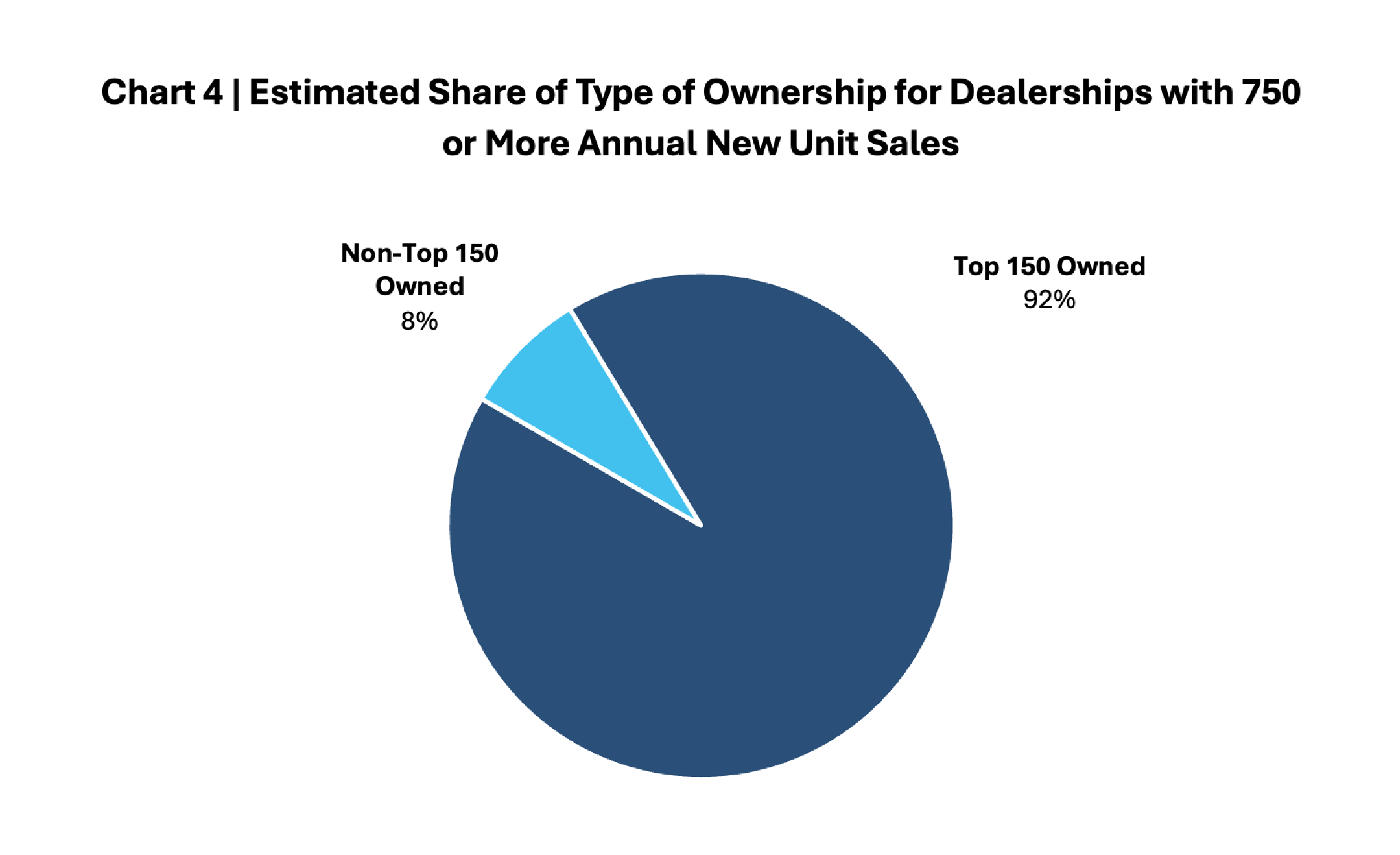

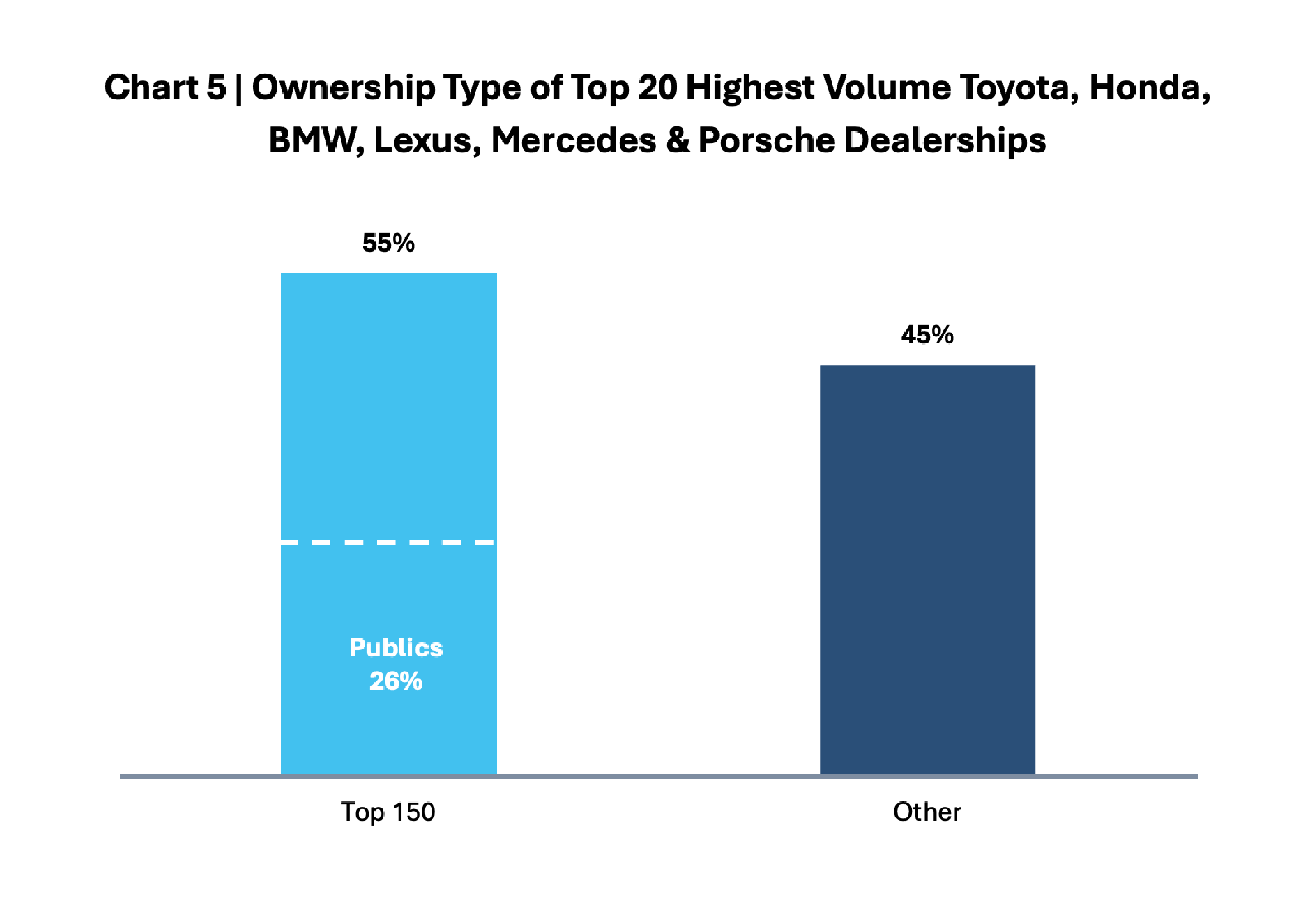

Like Lithia, most of the Top 150 dealership groups are also seeking to acquire higher volume dealerships. Collectively, the Top 150 already own 4,800+ dealerships that average 875+ new vehicle sales per rooftop, 10% above the industry average. Kerrigan Advisors estimates that 92% of the higher volume dealerships (those selling greater than 750 new vehicles per year) are already owned by the Top 150 (see Chart 4). That leaves just 8% or approximately 450 higher volume dealerships available for acquisition by growing groups seeking to scale into the Top 150 (see Chart 5). To further highlight the consolidated nature of the highest volume dealerships, the majority of the top 20 highest-volume dealerships for the top franchises (Toyota, Honda, BMW, Lexus, Mercedes & Porsche) are already majority owned by the Top 150 (see Chart 5), leaving a shrinking pool available for acquisition.

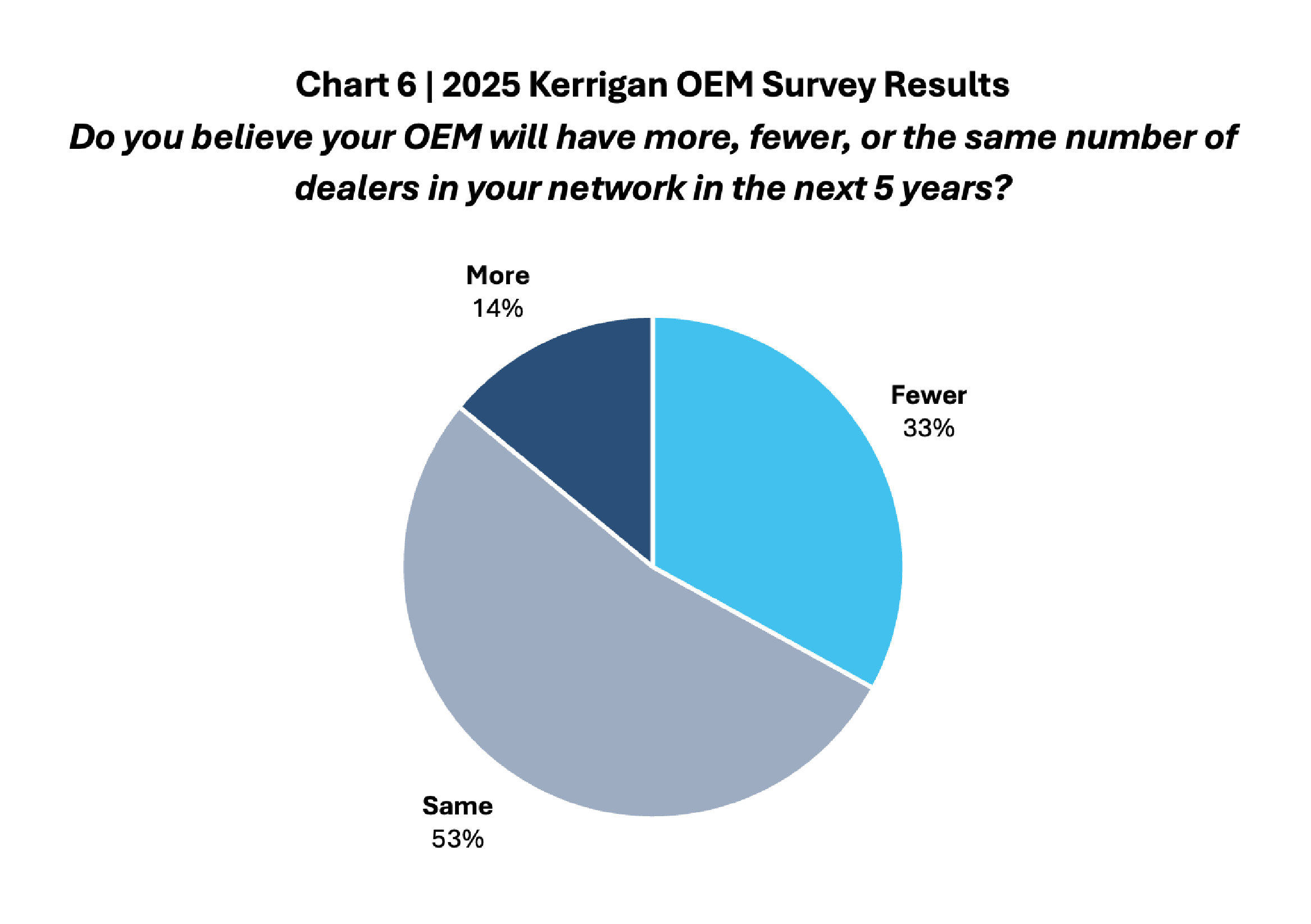

The scarcity of higher-volume dealerships for purchase is contributing to a greater dispersion of valuations by franchise today. Higher volume dealerships, particularly top brands, are in high demand by leading consolidators, resulting in price premiums, while dealerships with lower sales volumes representing weaker brands are more difficult to sell with fewer interested buyers. OEM expectations are also reinforcing this dynamic. According to Kerrigan Advisors’ OEM Survey, 33% of manufacturers anticipate fewer dealers within their networks over the next five years (see Chart 6), demonstrating their bias toward fewer, higher volume franchises. Based on the increasingly significant facility investment expectations of many OEMs, there is an inherent preference toward higher volume franchises that can support these significant embedded fixed costs.

Competitive signals from outside the traditional dealership franchise model further highlight the importance of throughput per rooftop. Carvana, the newest entrant to the new auto retail market, has demonstrated its ability to retail 15,000 vehicles from a single location, illustrating the productivity potential of a centralized, technology-enabled retail model. While franchise dealerships operate under some different structural constraints from Carvana, the broader message is clear: revenue per rooftop will increasingly determine competitive success in an emerging technology-driven retail environment.

Kerrigan Advisors is the leading sell-side advisor and thought partner to auto dealers nationwide. Since its founding in 2014, the firm has led the industry with the sale of more than 445 franchises generating more than $10 billion in client proceeds, including two of the largest transactions in auto retail history – the sale of Jim Koons Automotive Companies to Asbury Automotive Group and Leith Automotive to Holman. The firm advises the industry’s leading dealership groups, enhancing value through the lifecycle of growing, operating and, when the time is right, selling their businesses. Led by a team of veteran industry experts with backgrounds in investment banking, private equity, accounting, finance and real estate, Kerrigan Advisors is the only firm in auto retail exclusively dedicated to sell-side advisory, providing its clients the assurance of a conflict-free approach.

Kerrigan Advisors monitors conditions in the buy/sell market and publishes an in-depth analysis each quarter in The Blue Sky Report®, the industry authority on dealership buy/sell market trends and valuations and includes Kerrigan Advisors’ signature blue sky charts, multiples and analysis for each franchise in the luxury and non-luxury segments. To download a preview of the report, click here. The firm also releases The Kerrigan Index™ comprised of the seven publicly traded auto retail companies with operations focused on the US market. The Kerrigan Auto Retail Index is designed to track dealership valuation trends, while also providing key insights into factors influencing auto retail. To access The Kerrigan Index™, click here. To read the 2025 Kerrigan Dealer Survey, click here. To read the 2025 Kerrigan OEM Survey, click here. Kerrigan Advisors also is the co-author of NADA’s Guide to Buying and Selling a Dealership.

Contact us to learn more about Kerrigan Advisors’ sell-side services.

All of our conversations are 100% confidential.